What Will Cause the Next Recession?

News

|

Posted 18/05/2018

|

11481

Below are two ‘must read’ articles by respected analysts. They are reasonably short but maybe ones to read over the weekend. Both are concerning the terminal nature of this debt fuelled cycle. The first from a corporate perspective and the second at the public level.

If you don’t have the time, your 30 second summary is:

John Maudlin writes of the ‘new norm’ where crashes are brought about by credit cycles not economic cycles. Pre 80’s we saw economic cycle recessions cause sharemarket crashes. Since then we have seen credit cycles ending, causing sharemarkets to crash, leading to a recession. i.e. remove the debt fuelled stimulus, the cycle ends and the rush for the tiny exit door leads to chaos. He presents a chart showing very clearly we are at the top of the current corporate debt cycle and talks to a “liquidity crisis of biblical proportions” when those funders go to exit.

Simon Black talks to the quite staggering accumulation of US debt in a “financial death spiral” scenario. Whilst regular readers are not alien to the US Debt issue, Simon paints a clear picture of the fatal combination of the steepening trajectory of their debt balance coinciding with now clear upward moves in interest rates and no ability to simply change course.

So first, John Maudlin:

A Liquidity Crisis of Biblical Proportions Is Upon Us

Last week, I mentioned an insightful comment my friend Peter Boockvar—CIO of Bleakley Advisory Group—made at dinner in New York: “We now have credit cycles instead of economic cycles.”

That one sentence provoked numerous phone calls and emails, all seeking elaboration. What did Peter mean by that statement?

In an old-style economic cycle, recessions triggered bear markets. Economic contraction slowed consumer spending, corporate earnings fell, and stock prices dropped. That’s not how it works when the credit cycle is in control.

Lower asset prices aren’t the result of a recession. They cause the recession. That’s because access to credit drives consumer spending and business investment.

Take it away and they decline. Recession follows.

The Illusion of Liquidity

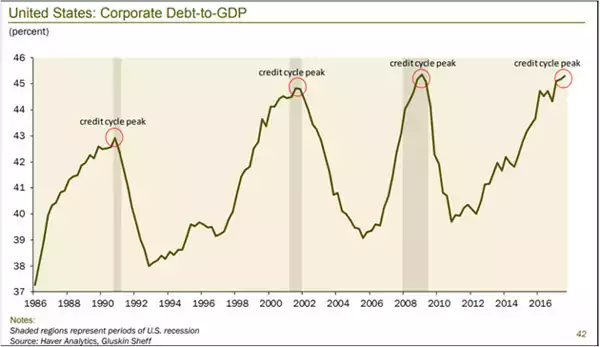

Corporate debt is now at a level that has not ended well in past cycles. Here’s a chart from Dave Rosenberg:

The Debt/GDP ratio could go higher still, but I think not much more. Whenever it falls, lenders (including bond fund and ETF investors) will want to sell. Then comes the hard part: to whom?

You see, it’s not just borrowers who’ve become accustomed to easy credit. Many lenders assume they can exit at a moment’s notice. One reason for the Great Recession was so many borrowers had sold short-term commercial paper to buy long-term assets.

Things got worse when they couldn’t roll over the debt and some are now doing exactly the same thing again, except in much riskier high-yield debt. We have two related problems here.

- Corporate debt and especially high-yield debt issuance has exploded since 2009.

- Tighter regulations discouraged banks from making markets in corporate and HY debt.

Both are problems but the second is worse. Experts tell me that Dodd-Frank requirements have reduced major bank market-making abilities by around 90%. For now, bond market liquidity is fine because hedge funds and other non-bank lenders have filled the gap.

The problem is they are not true market makers. Nothing requires them to hold inventory or buy when you want to sell. That means all the bids can “magically” disappear just when you need them most.

These “shadow banks” are not in the business of protecting your assets. They are worried about their own profits and those of their clients.

Gavekal’s Louis Gave wrote a fascinating article on this last week titled, “The Illusion of Liquidity and Its Consequences.” He pulled the numbers on corporate bond ETFs and compared them to the inventory trading desks were holding—a rough measure of liquidity.

Louis found dealer inventory is not remotely enough to accommodate the selling he expects as higher rates bite more.

‘We now have a corporate bond market that has roughly doubled in size while the willingness and ability of bond dealers to provide liquidity into a stressed market has fallen by more than -80%. At the same time, this market has a brand-new class of investors, who are likely to expect daily liquidity if and when market behavior turns sour. At the very least, it is clear that this is a very different corporate bond market and history-based financial models will most likely be found wanting.’

The “new class” of investors he mentions are corporate bond ETF and mutual fund shareholders. These funds have exploded in size (high yield alone is now around $2 trillion) and their design presumes a market with ample liquidity.

We barely have such a market right now, and we certainly won’t have one after rates jump another 50–100 basis points.

Worse, I don’t have enough exclamation points to describe the disaster when high-yield funds, often purchased by mom-and-pop investors in a reach for yield, all try to sell at once, and the funds sell anything they can at fire-sale prices to meet redemptions.

In a bear market you sell what you can, not what you want to. We will look at what happens to high-yield funds in bear markets in a later letter. The picture is not pretty.

Leverage, Leverage, Leverage

To make matters worse, many of these lenders are far more leveraged this time. They bought their corporate bonds with borrowed money, confident that low interest rates and defaults would keep risks manageable.

In fact, according to S&P Global Market Watch, 77% of corporate bonds that are leveraged are what’s known as “covenant-lite.” That means the borrower doesn’t have to repay by conventional means.

Somehow, lenders thought it was a good idea to buy those bonds. Maybe that made sense in good times. In bad times? It can precipitate a crisis. As the economy enters recession, many companies will lose their ability to service debt, especially now that the Fed is making it more expensive to roll over—as multiple trillions of dollars will need to do in the next few years.

Normally this would be the borrowers’ problem, but covenant-lite lenders took it on themselves.

The macroeconomic effects will spread even more widely. Companies that can’t service their debt have little choice but to shrink. They will do it via layoffs, reducing inventory and investment, or selling assets.

All those reduce growth and, if widespread enough, lead to recession.

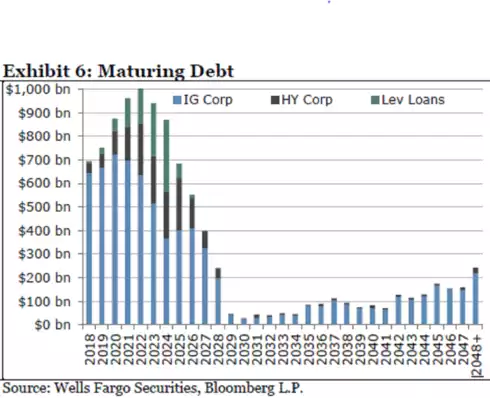

Let’s look at this data and troubling chart from Bloomberg:

‘Companies will need to refinance an estimated $4 trillion of bonds over the next five years, about two-thirds of all their outstanding debt, according to Wells Fargo Securities. This has investors concerned because rising rates means it will cost more to pay for unprecedented amounts of borrowing, which could push balance sheets toward a tipping point. And on top of that, many see the economy slowing down at the same time the rollovers are peaking.

“If more of your cash flow is spent into servicing your debt and not trying to grow your company, that could, over time—if enough companies are doing that—lead to economic contraction,” said Zachary Chavis, a portfolio manager at Sage Advisory Services Ltd. in Austin, Texas. “A lot of people are worried that could happen in the next two years.” ’

The problem is that much of the $2 trillion in bond ETF and mutual funds isn’t owned by long-term investors who hold maturity. When the herd of investors calls up to redeem, there will be no bids for their “bad” bonds.

But they’re required to pay redemptions, so they’ll have to sell their “good” bonds. Remaining investors will be stuck with an increasingly poor-quality portfolio, which will drop even faster.

Wash, rinse, repeat. Those of us with a little gray hair have seen this before, but I think the coming one is potentially biblical in proportion.

And now Simon Black:

Breaking down America’s worst long-term challenges: #1- Debt.

On October 22, 1981, the national debt in the United States crossed the $1 trillion threshold for the first time in history.

It took nearly two centuries to reach that unfortunate milestone.

And over that time the country had been through a revolution, civil war, two world wars, the Great Depression, the nuclear arms race… plus dozens of other wars, financial panics, and economic crises.

Today, the national debt stands at more than $21 trillion– a milestone hit roughly two months ago.

This means that the government added $20 trillion to the national debt in the 37 years between October 22, 1981 and March 15, 2018.

That’s an average of nearly $1.5 BILLION added to the national debt every single day… $62 million per hour… $1 million per minute… and more than $17,000 per SECOND.

But the problem for the US government is that this trend has grown worse over the years.

It took only 214 days for the government to go from $20 trillion in debt to $21 trillion in debt– less than eight months to add a trillion dollars to the national debt.

That’s an average of almost $52,000 per second.

Think about that: on average, the US national debt increases by more in a split second than the typical American worker earns in an entire year.

And there is no end in sight.

At 105% of GDP, America’s national debt is already larger than the size of the entire US economy. (By comparison the national debt was just 31% of GDP in 1981.)

Plus, the government’s own projections show a steep increase to the debt in the coming years and decades.

The Treasury Department has already estimated that it will borrow $1 trillion this fiscal year, $1 trillion next year, and another trillion dollars the year after that.

They’re also forecasting the national debt to exceed $30 trillion by 2025.

To be fair, debt isn’t always bad. In fact, sometimes debt can be useful.

Businesses and individuals use debt all the time to shrewdly finance productive investments.

Real estate investors, for instance, often borrow most of the money they need to purchase a property once they determine that the rental income should more than cover the debt service.

In this way, when applied prudently, debt can actually help build wealth.

And the US federal government did the same thing in its early history.

It was an incredibly astute move on the government’s part, for example, to go into debt to finance the Louisiana Purchase back in the early 1800s, which dramatically expanded the size of the budding nation.

These days, however, the government flushes money down the toilet in the most wasteful ways imaginable, both big and small.

We’ve covered some of the more ridiculous examples in our normal conversations, from that $2 billion Obamacare website to the $856,000 that the National Science Foundation spent teaching mountain lions to run on treadmills.

Even the government’s more legitimate expenses are absolutely colossal now.

Last year the government spent HALF of its budget just to pay for Social Security and Medicare.

The situation is so dire that the government spends more than its entire tax revenue just on these mandatory entitlement programs, plus Defense and interest on the debt.

Even if you could eliminate entire departments of government, they would still be running a budget deficit and going deeper into debt.

The larger the national debt becomes, the more interest the government has to pay each year.

And interest payments increase even more rapidly as rates continue to rise… which is exactly what’s happening now.

A few years ago, the government paid less than 1.5% on its 10-year Treasury note. Today the rate has doubled.

This has a profound impact on Uncle Sam’s cash flow: they have to borrow MORE money just to pay interest on the money they’ve already borrowed… and spend a larger and larger share of the budget on debt service.

It’s a financial death spiral.

Think about it: if the government is having this much trouble making ends meet when they’re paying 2% interest on $21 trillion in debt, what’s going to happen when they’re paying 5% on $30 trillion?

It’s foolish to think that this trend has a consequence-free outcome. No nation in history has ever become prosperous by borrowing record amounts of debt to finance reckless spending.

Us again now… If you don’t have an SMSF and have been told you don’t have enough in your super to ‘allow’ you to do one, and you missed reading yesterday’s news, we suggest you do so. Click here to go there.