Is a War Coming with China?

News

|

Posted 12/10/2018

|

9324

Let’s first recap another tumultuous night on global markets. On Wall Street the Dow ended down another 546 points (2.1%) but was down almost 700 points and below its 200 DMA before a rebound on news that Trump and Xi agreed to meet at the G20 to discuss trade. That bounce was short lived though and the Dow now sits 1,950 points below its highs just last week. The S&P500 extended its losses to 6 straight days, down another 57 points or 2.1% and below its 200 DMA. The NASDAQ was down 93 points (1.3%), still below its 200 DMA and as at just the 11th day of the month, already its worst month since GFC onset November 2008. China’s Shanghai Composite was down 142 points (5.2%) with around 1,000 companies halted 10% limit down and taking the year to date losses below 20% and lows not seen since November 2014. For context at 2,583 it is still less than half its pre GFC high of 6092. Japan’s Nikkei was down 915 (3.9%). Lead by Italy which is now officially in a bear market (down >20%) Euro stocks fell further with the Europe 500 index now down 7% for the year to levels not seen since 2016. At home we saw the ASX200 down 166 points (2.7%) yesterday and the futures market indicating more pain at the open today.

Gold and Silver? Over the last 24 hours (Aussie + Northern Hemisphere financial markets) saw gold up US$34 / AU$37 (2.8%) and silver up $US0.37 / AU$0.42 (2.6%). As we discussed yesterday, that safe haven go-to lack of correlation is playing out very nicely right now.

As last night demonstrated again (with that rebound in the Dow) the market is rightly nervous about the growing tensions between the world’s two superpowers. You won’t have any trouble finding plenty of sensationalist stories around this but, to be honest, many of them are from questionable sources and many in the doomsday camp. And that is why we feel compelled to share the following article penned by Ray Dalio, head of the world’s largest hedge fund and arguably the ‘king of Wall St’. Mr Dalio is certainly one to listen to when he breaks from ‘safe’ mainstream doctrine. Before throwing to him, please remember the context of China holding the world’s largest stash of US Treasuries, nearly $1.2 trillion worth. Imagine the carnage should they dump them on the market in a retaliatory move. That would simply and quickly kill the USD. So the fact that they also hold the world’s largest stash of physical gold is an important part of that equation in terms of their hedge. Australia is in an unenviable and precarious position in this US v China equation. Our economy is completely beholden to China but our age old ally is the US. Rock meet hard place… This is a must read for any global citizen.

“The “War” with China Is Spreading

Background

Because geopolitics is playing a greater role in driving economies and markets than any time in my over 50 years of investing, I am thinking a lot more about it. As you know, I believe that:

a) most important things happen over and over again in basically the same ways because the most fundamental cause-effect relationships are timeless and universal (and logical), and

b) right now conflicts both within countries and between countries are increasing because of increased wealth/income/opportunity gaps, diverging values, and rising powers (most importantly China) emerging to challenge existing powers (most importantly the US).

As in the past, these conditions are leading to the rise of populism, which is leading to important policy shifts to influence economic outcomes (like tariffs, economic sanctions, capital controls, big corporate tax cuts, etc.) that are having big market implications.

Conflicts are increasing within countries as the number of confrontational populists from both the right and the left are increasing relative to the number of moderates who are more inclined to find compromises to bring about unity. At the same time, conflicts are increasing between countries a) because these populist leaders are more nationalistic and are more willing to fight than the globalists who are more inclined to seek cooperation, and b) because countries (most importantly China) are challenging US dominance.

These conditions now exist:

a) in the later stage of the short-term debt cycle (nine years in) when slack is limited and central banks are shifting from being stimulative to being restrictive, and

b) in the later stage of the long-term debt cycle when debt and non-debt obligations (like pension and healthcare obligations) are high, interest rates are near 0%, and printing money to buy financial assets will have a reduced stimulative effect.

This risky configuration of circumstances has occurred numerous past times, most recently in the late 1930s.

Update

Around 18 months ago, we did a study on populism (attached), which helped us to better understand it and led us to focus on how conflicts are being handled because that was the single most important indicator of how events would transpire. The most important international conflict is between the US and China, so we have been monitoring it closely. As the title conveys, this conflict is spreading beyond trade. Notable recent developments include:

On September 20, the US sanctioned the branch of China’s military that is responsible for weapons procurement as well as the individual who is responsible for it (Lt. Gen. Li Shangfu). The 2017 US law, which created the economic sanctions weapon (called the Countering America’s Adversaries Through Sanctions Act), was in large part put into place to punish Russia for aggression in Ukraine and was used to punish Russia for allegedly meddling in US elections and objectionable actions in Syria’s civil war. Using it to hit China with sanctions was a new type of aggressive, non-trade-related act.

That led to a strong verbal reaction from China in the form of issuing a statement on September 22 from the defense ministry that said that the US had “no right to interfere,” and that “The US approach is a blatant violation of the basic norms of international relations, a full manifestation of hegemony, and a serious breach of the relations between the two countries and their two militaries.”

On September 24, the US announced that it would sell $330 million worth of military and aircraft parts to Taiwan, which led to China’s September 25 expression of “strong dissatisfaction and firm opposition” to the sale, saying it “severely violates” international law and that the deal could “cause severe damage to US-China relations.”

On September 25, China denied a request for a US carrier strike group led by the USS John C. Stennis to visit Hong Kong.

On September 26, President Trump charged China with trying to influence midterm elections, raising the possibility that he will use that perspective to further raise sanctions on China as he did on Russia for allegedly trying to influence elections.

On September 30, a Chinese warship came within 45 yards of a US warship, forcing it to change course to avoid collision. The warships were patrolling in the Spratly Islands, a group of islands in the South China Sea that China claims sovereignty over, but other countries dispute that claim. The Pentagon described the Chinese moves as “a series of increasingly aggressive maneuvers.” A spokesman for China’s Ministry of National Defense said, “The United States has repeatedly sent military ships to South China Sea islands and its adjacent waters, threatened China’s sovereignty and security, seriously damaged the relations between the two countries and militaries, and endangered regional peace and stability.”

On October 1, a visit to Beijing by Defense Secretary Mattis to discuss security issues with his Chinese counterparts was cancelled just before the trip. This suspends the only active US-China bilateral dialogues between the governments (there are three other inactive ones).

On October 4, Bloomberg reported that China’s People’s Liberation Army inserted a tiny espionage chip into motherboards of servers to spy on a number of big company and government servers. The chips, around the size of a grain of rice, were installed by manufacturing subcontractors to the US producer of motherboards Supermicro. The chips allowed intruders to have the motherboards communicate with outside computers to get code that could then be inserted into the operating system, leaving an opening for attackers and spies.

On October 4, Vice President Pence gave a speech describing the “great-power competition” in which he said that “Chinese security agencies have masterminded the wholesale theft of American technology” and that “China has initiated an unprecedented effort to influence American public opinion, the 2018 elections, and the environment leading into the 2020 presidential elections.” He went on to say that “Beijing is also using its power like never before. China now spends as much on its military as the rest of Asia combined, and is prioritizing capabilities to erode US military advantages on land, at sea, in the air, and in space.” Understandably, he did not mention US military activities, spending, and borrowing to support these activities or China’s role in lending to the US to support these things.

On October 10, the Treasury Department said that it will be using new powers that Congress gave it earlier this year when it passed the Foreign Investment Risk Review Modernization Act to more strictly review Chinese investment in the US technology area.

On October 10, Justice Department officials announced that a Chinese intelligence official had been extradited to the US to face espionage charges after being arrested in Belgium. This was a move to a more aggressive posture, as such an action was unprecedented.

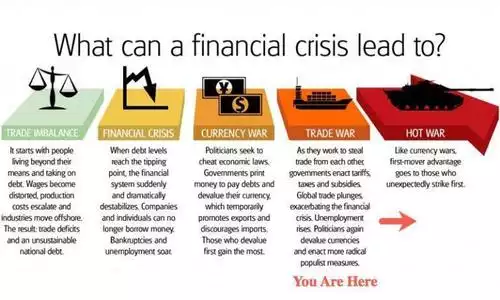

It should now be clear to everyone that this is not just a trade war. Where exactly this broader confrontation/war leads is unknown to anyone, including the policy makers who are setting policy.

We can visualize a wide range of scenarios - ranging from a conflict limited to tariffs that would raise inflation and lower growth a bit, to a much more serious conflict that disrupts supply lines in ways that have big negative impacts on companies’ efficiencies and profits, to the US prohibiting important technologies built in China from coming into the US (or vice versa) and other products (like luxury brands) that hurt these companies, to a capital war in which China boycotts or sells treasuries, to there being a testing of each other militarily.

While there will be ebbs and flows in the relationship, as far as the symmetry of the surprises goes, it seems to me that they are more asymmetrical on the downside relative to what the market is discounting. As this is happening in the later stages of both the short-term and long-term debt cycles while central banks are tightening with the duration of assets long (because interest rates are so low), this is an environment in which we prefer to have a risk-off posture.”