The Australian Property Dilemma

News

|

Posted 07/06/2018

|

8756

This week saw more concerning news from the ‘bullet proof’ Aussie property market.

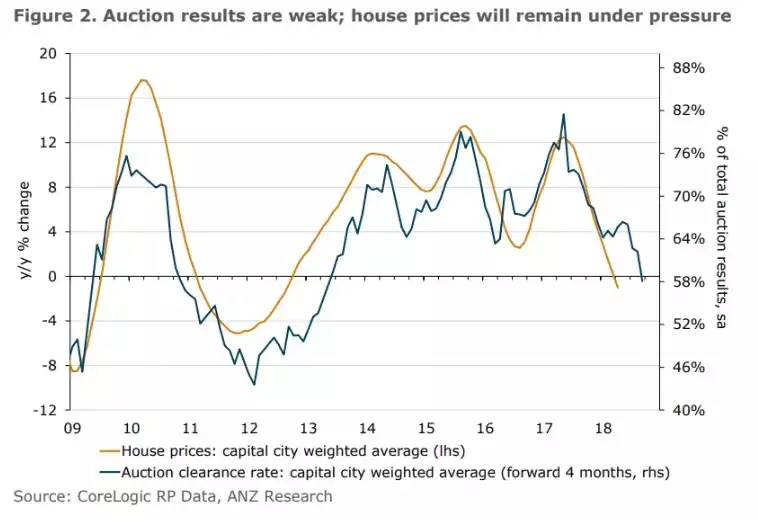

Home prices fell for an eighth consecutive month in May, dragged lower once again by weakness in Sydney and Melbourne. CoreLogic’s Home Value Index saw national dwelling values slip 0.1%, with house prices falling 0.1% and apartments down 0.3% over the month and taking the yearly figure to minus 0.4%, the first decline seen since October 2012. Prices peaked in September 2017 and are now down 1.1% and falling. Only 3 states posted gains, with the rest in decline.

Unsurprisingly Auction clearance rates are at multi-year lows, and housing credit growth, particularly to investors, is slowing fast, reflecting restrictions on interest-only lending from Australia’s banking regulator, APRA.

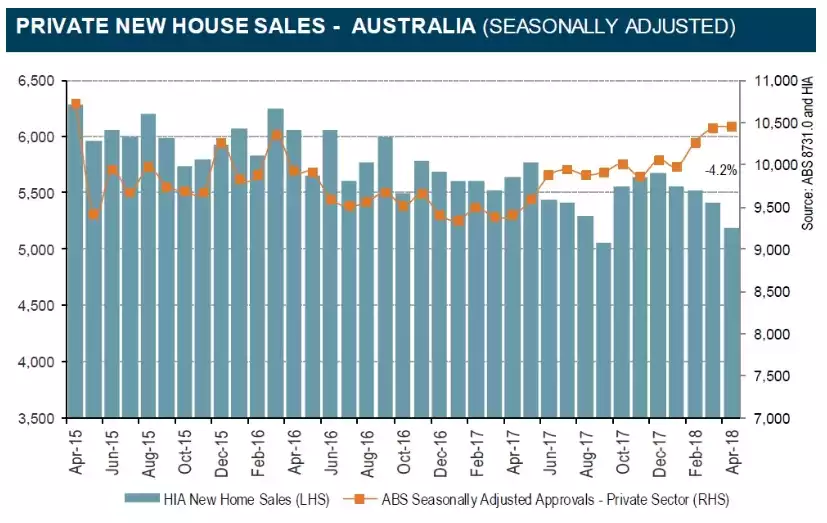

Australia’s Housing Industry Association (HIA) also released their sales of new detached houses data, seeing a 4.2% decline and 3.1% down over the year. Unlike the split price declines, sales fell in each of Australia’s mainland states, led by declines of 11.6% in Western Australia and 8.2% in New South Wales.

Much of the blame lies with the tighter lending practices forced by APRA, particularly on investors and the tighter controls on Chinese investors.

According to Tim Reardon, principal economist at the HIA:

“The value of housing loans to investors peaked in August 2017 at $152.7 billion in the preceding 12 months…..Since then investor loans have been falling quite steadily to $144.2 billion over the year to March 2018, representing a reduction of 5.6% on last August’s peak.”

According to Australia’s Foreign Investment Review Board (FIRB), applications from foreigners (who almost exclusively buy new dwellings) plummeted from 50,149 in FY16 to 13,198 in FY17.

First Home buyer sales have also slowed after the stimulus bump last year of stamp duty discounts introduced by the New South Wales and Victorian state governments.

That latter point is an important one to the broader picture of Aussie property. Our government is hell-bent on keeping property going. The obvious tactics are first home buyer grants and negative gearing. However it goes well beyond that and the ABC wrote an insightful article recently titled “Why Australia's governments, banks and economy don't want 'affordable' housing”.

“There are only two things that keep senior Reserve Bank officials awake at night; China and Australian real estate.

RBA boss Philip Lowe has become increasingly vocal about China's massive debt mountain and the dangers it poses for Australia should it implode.

But our housing market is equally as unnerving. Our major banks have a decidedly unhealthy exposure to domestic real estate, with up to 60 per cent of their total loans allocated to Australian mortgages.

After being burnt by big business in the 1987 stock market meltdown, they decided en masse that real estate was a safer option and poured trillions of dollars into home loans, which we consumers happily lapped up.

Having splurged so much on homes, our household debt, at just shy of 200 per cent of annual income, ranks among the world's highest. Hocked to the eyeballs, it's no wonder our household consumption is sluggish, retail sales are struggling and inflation is anaemic.

The problem is, if Australian real estate declines in any significant way, it will put a serious handbrake on the economy.”

But this is not just a banking thing, all levels of government have also used the property market to come to the rescue post mining boom (refer earlier RBA fixation with China…).

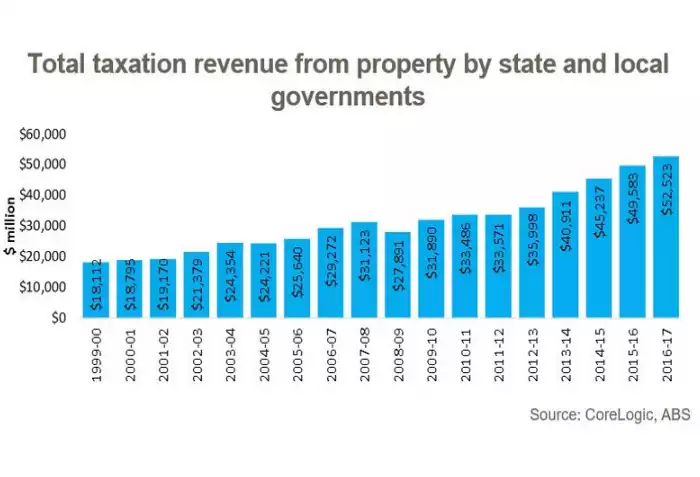

“The Federal Government needs rising property prices to maintain a stable economy while state and local governments feed off the enormous fees and taxes it generates.

Since the latest boom began in late 2012, a boom deliberately orchestrated by the Reserve Bank to absorb construction workers leaving the mining industry as the resource investment boom wound down, state and local governments have seen property revenues rise by 65 per cent.”

That article then goes on to talk about how the government pulls the property levers and it worth repeating verbatim as it completely sums up the Aussie dilemma of population growth and the ‘growth trap’ more broadly…

“While some bears have been predicting a crash in Australian housing for decades, the chances have increased significantly in the past 18 months.

Global interest rates are on the rise which eventually will feed through to Australia and could put a significant number of households under stress, leading to higher defaults and lower property prices. Then there's the clampdown on foreign ownership, particularly Chinese investors, who were skirting the law.

But the biggest concern has been supply. The building boom, particularly in the eastern capitals of Brisbane, Sydney and Melbourne has been unprecedented, much of it in high rise apartments.

Cranes dot the skies above our eastern capitals like never before. In fact, Sydney — which accounts for half the cranes across the nation — alone has the equivalent of 80 per cent of the cranes across all of North America.

Melbourne has a little less than half that of Sydney. In both cities, cranes for residential construction at last have begun to decline.

Instead there has been a dramatic pick-up in crane use for commercial and infrastructure use, as governments belatedly attempt to provide infrastructure to service the huge growth in population.

Therein lies the key as to why our property prices keep rising.

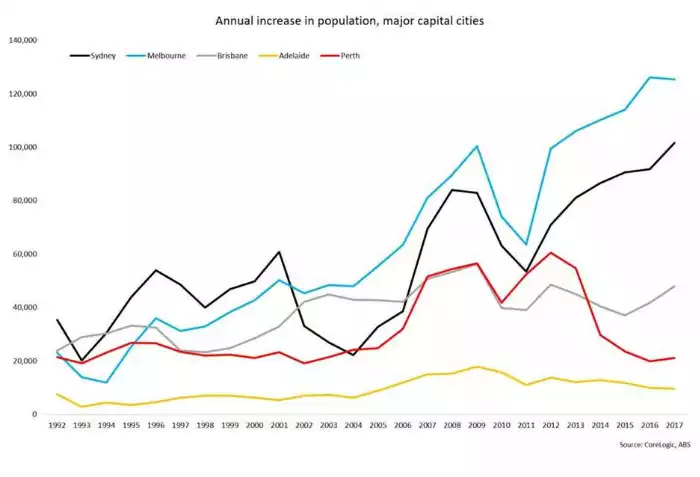

While our politicians bicker and argue about border control and handfuls of refugees, Australia quietly has run one of the biggest immigration programs of any developed nation.

Our population has been growing at around 1.6 per cent per annum, second only to New Zealand and well above the OECD average of 0.7 per cent.

While there's nothing wrong with immigration, particularly if there is a need for a rapid lift in population, our large and growing intake has been used to give the impression that our economy has been travelling better than it appears.

While we are about to run up 27 years of uninterrupted economic growth on a national basis, as individuals, many of us are worse off. Wages growth is stagnant because, for all the claims of job creation, we're barely standing still if you take the new arrivals into account.

When it comes to property prices, population growth has been every federal government's secret weapon.

For years, we've been told our skyrocketing housing costs has been a supply problem. Instead, there has been a deliberate effort to keep piling on the demand, just to maintain the illusion of economic growth and to keep the real estate sales clicking over.”

And therein lies the multi levelled dilemma of a Ponzi-esque growth at all costs agenda, the erosion of the very fundamentals of the Aussie dream, and the ballooning debt that sits behind it all.