Record Inflow to Gold ETFs in Perspective

News

|

Posted 05/07/2016

|

4863

Two items of investment data came out in the last week that paint a picture of investors starting to get what’s coming. Firstly we saw the Global Hedge Fund Index lose 1.1% up to 29 June this year. That makes the first half of 2016 the worst year for so called ‘smart money’ since the first half of 2011 when they lost 2.1%. We reported yesterday on what happened to silver (and gold followed) in that first half of 2011. History repeating?

Yesterday Bloomberg reported that Gold ETF’s (share traded gold) saw more than 500 tonne added since the price bottomed at the beginning of the year. On Friday, as everyone was transfixed on silver’s meteoric rise, the gold ETF’s saw the biggest single day inflow ever, with a whopping $263m.

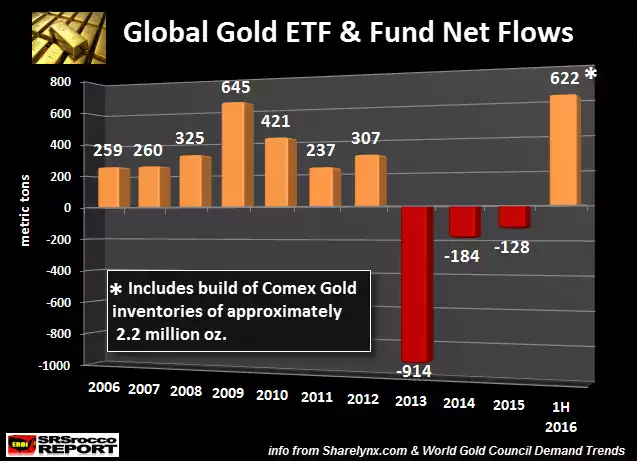

SRSRocco estimate that 500t as closer to 550t and in the chart below add the 68t of gold added to COMEX inventories to show a total global gold ETF and fund net inflow of 622 tonne. As you can see that has only been surpassed by the full year inflows of GFC 2009.

To put that 622 tonne (20m oz) into perspective:

- 622 tonne represents 41% of total global gold production over that period;

- After that surge we have total gold ETF’s & Funds worth around $108 billion and the same for silver worth around $16 billion, totalling $124 billion of ‘paper’ and mostly leveraged gold and silver. On the Friday after Brexit the world’s 400 richest people lost $127 billion. i.e. that could have bought ALL the ‘paper’ gold and silver in the world.

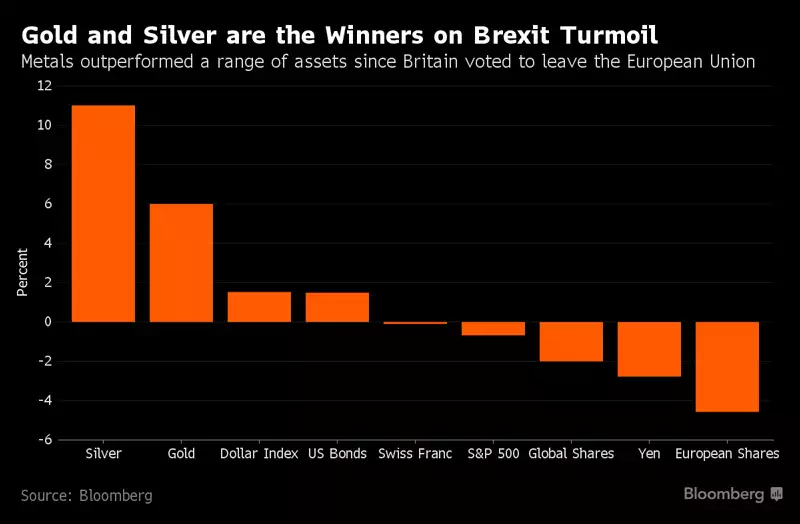

This latter point is critical as it reinforces what we try to get across in terms of the size of financial markets and the size of the gold and silver market. When even a fraction of that market tries to get into gold and silver it can be very quickly and completely be overwhelmed. Those with physical gold and silver (not ‘paper’) will be the big winners. When more and more mainstream investors see charts like the one below from Bloomberg’s, the momentum we have seen thus far in 2016 can increase exponentially.