“Stagflation is Here” – CPI overshoots & Fed confirms taper

News

|

Posted 14/10/2021

|

8850

Last night we saw both the latest CPI print out of the US together with the minutes from the last Fed meeting. Combined they paint a very clear concern around the stagflation we discussed yesterday. Gold surged over $35 and silver over 50c on the news after an initial reflexive dip.

As the Bloomberg headline eloquently put it “U.S. Consumer Prices Outpace Forecast as Inflation Dogs Economy” with a 0.4% increase to 5.4% annualised smashing expectations. This combined with the Fed minutes confirming their fears of sustained (not transitory) inflation outweighed the weak economy and seeing them almost certainly starting to taper from November and announce that at the next meeting on 2-3 November. Of course there has been the weak NFP jobs report since, but last night’s CPI print has pretty much cemented the outcome. HOWEVER…. The taper is just $15b/month off the whopping $120b/month and they openly state the economy is too weak to raise rates for ‘years’. A taper may well serve only to crash markets and little to stem inflation….

The excerpts below from the latest investor newsletter from Crescat is maybe as good an outline of the situation as you will read. Whilst we have reduced it, it is still longer than our usual news but is certainly worth reading in full when you have a chance. If you haven’t read yesterday’s news, that is a must read too to understand how assets perform in stagflationary environments.

“Stagflation is Here

The problem is that while consumer prices are rising, we are also seeing signs that the global economy is starting to decelerate. China is the elephant in the room in that respect. The second largest economy in the world has achieved that spot while creating a property and credit bubble that, as measured by banking assets to GDP, is more than four times the size of the US housing and financial sector bubble ahead of the GFC. With its equity markets under pressure since February, the Evergrande collapse, and nationwide energy shortages, China’s economy appears to be in a serious meltdown. The spillover effects should not be underestimated. We need to start discounting now the ultimate new global fiscal and monetary stimulus that will be needed to counter China’s currently unfolding credit collapse and what that portends for its currency given its communist banking system with a whopping $52 trillion of suspiciously priced assets. As we have learned throughout the world in the post GFC era, the speed at which governments can create new central bank money is instantaneous. At the same time, and more than ever today, the speed at which countries can deliver the basic resources to meet their citizens’ needs is significantly impaired.

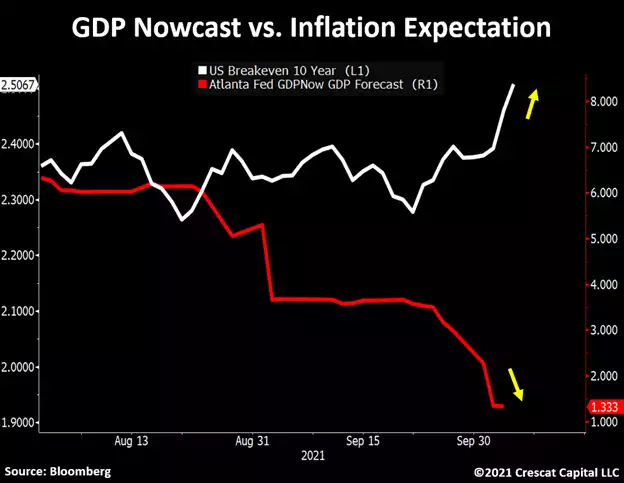

The US economy has already started to slow significantly. The Atlanta Fed GDP nowcast, for instance, just went from 6% to 1.3% in the last couple of months. With business activity now decelerating as inflation remains historically elevated, the set of monetary and fiscal policies needed to fix one problem would worsen the other. At the same time, with historic high valuations for equity and credit markets in the US at large, there is much downside risk. The Fed is trapped to do anything to prevent a rotation out of speculatively priced assets with deteriorating fundamentals.

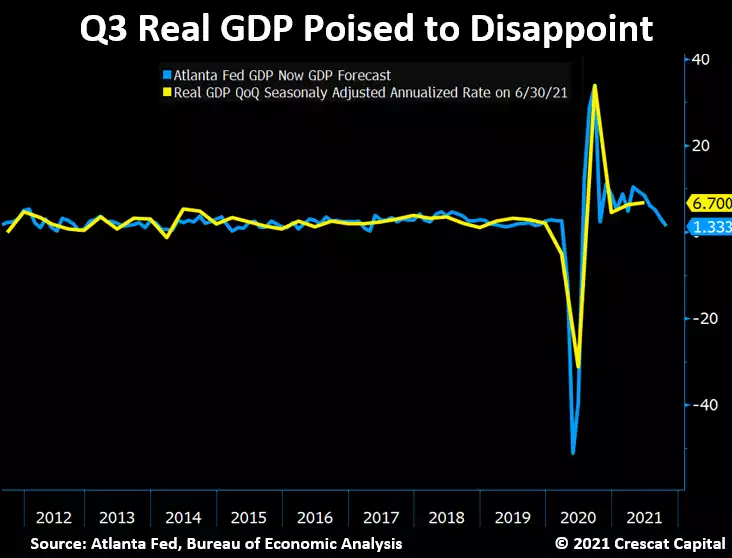

Note the tight correlation between the real-time Atlanta Fed’s macro quantitative measure of real GDP growth and actual subsequently reported economic growth after inflation.

Great Rotation

Financial markets are not correctly priced for the stagflation that is already evident in the macro data. This creates both risks and opportunities for a large swath of investors who are crowded on the wrong side of this trade in our view. First and foremost, we see a major shift out of overpriced growth stocks and fixed income securities and into a much narrower group of deeply undervalued and high near-term growth stocks and commodity investments that will be the primary beneficiaries of stagflation, creating a reflexive inflationary loop. The smart money should be the first to make this move. We call it the Great Rotation. The motivation for such a shift in our research is that it is the most highly probable way to both protect against the downside risk of significantly rising inflation to financial assets at large while potentially substantially profiting from it at the same time.

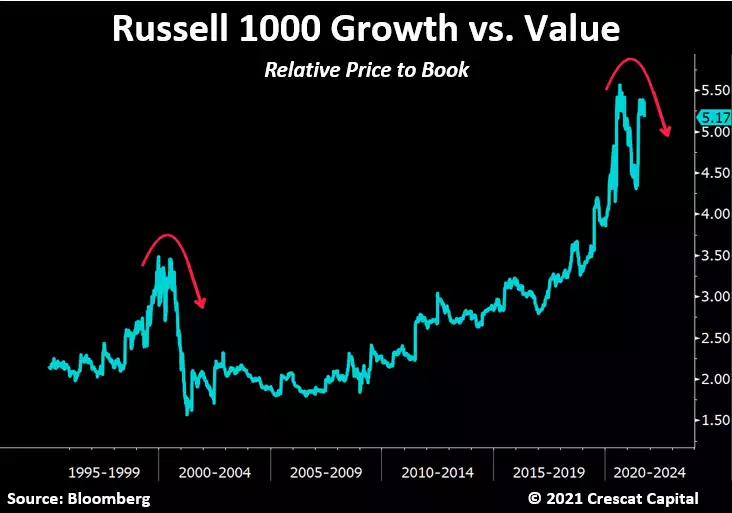

Investors should take note while overall price to book values for the broad market are at record highs along with many other fundamental measures, the relative price-to-book value of the Russell 1000 Growth compared to the Russell 1000 Value indices is about 60% higher than it was at the peak of the tech bubble in 2000, further illustrating the extreme imbalances and market risks along with the set-up for a growth to value rotation.

Getting Ahead with Gold and Silver

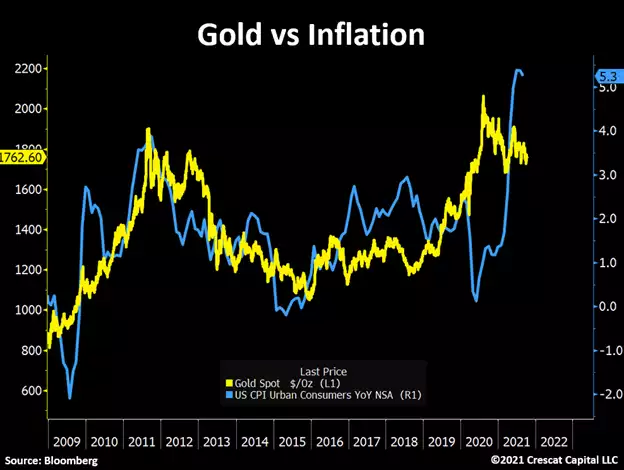

As inflation continues to develop in the economy, the chart below shows the incredible link between gold prices and CPI since the Global Financial Crisis. Note how after the pandemic lows, gold front ran the potential risk of a rise in consumer prices and the entire precious metals market appreciated sharply. Gold and silver not only diverged from CPI but also significantly outperformed the rest of the commodities market. It is important to remember that before recently peaking, gold had been going on a streak for two years already. The metal was up more than 75% from August 2018 to August 2020 and even reached historical highs during this period. Back then, with CPI around 1%, very few investors foresaw inflation as a risk to the economy. Now it is a real problem. We think gold likely appreciated too quick and too fast becoming what some thought as an obvious trade. Extreme sentiment probably explains the reason for its recent weakness after signaling way earlier than any other asset the possibility that an inflationary environment could be ahead of us. We are now on the other side of this extreme. Gold looks fundamentally cheap, technically oversold while inflation continues to gain traction. We think the historic relationship between precious metals and the growth in consumer prices will continue to be strong and the recent pullback in gold and silver related assets poses an incredible opportunity for investors to deploy capital at what we believe to be truly attractive levels. Also, keep in mind that we are using government reported numbers to gauge inflation in this analysis. We should all know by now that the true cost of goods and services is growing at a drastically faster pace than CPI.

Recent Pullback in Precious Metals Presents Constructive Buying Opportunity

We believe gold and silver commodity and equity markets are due for a major bull market resumption. This market may have already turned in our favor this month from deeply oversold levels for mining stocks and extreme negative sentiment despite incredibly positive fundamentals.”