Where’s the gold gone?

News

|

Posted 20/01/2015

|

6926

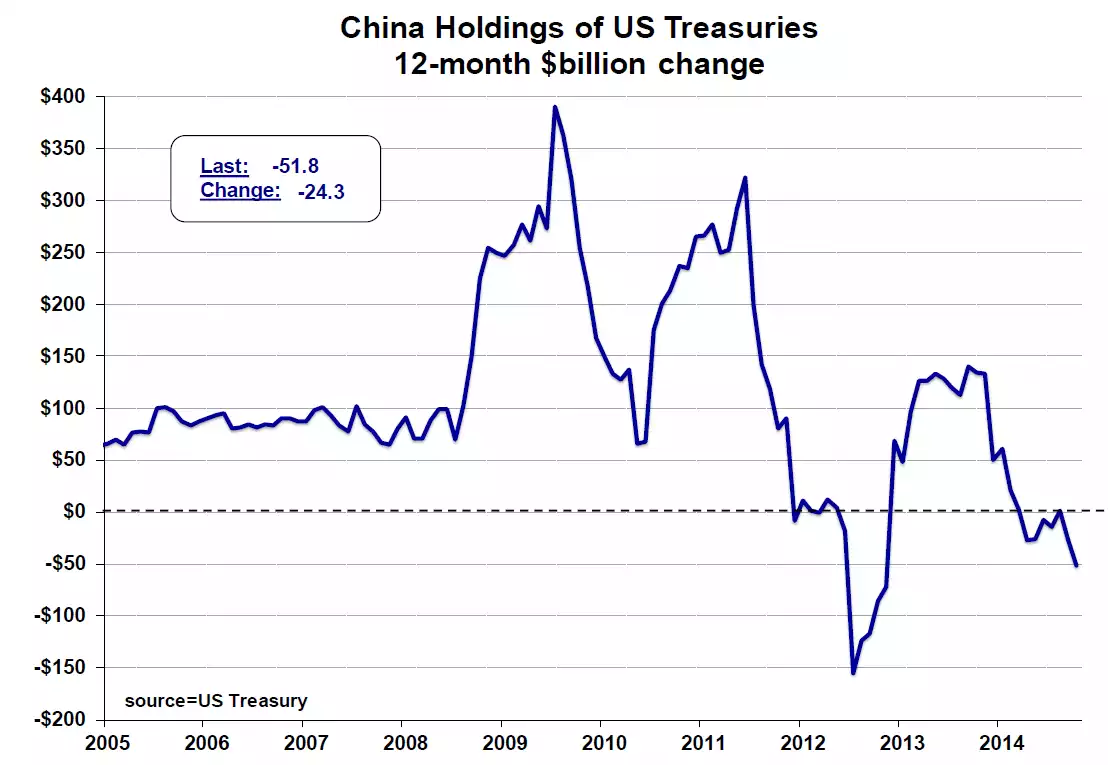

It is now well documented that just China and India alone accounted for all the global gold production in 2014, excluding Government purchases. That means the rest of the world is drawing down on reserves and recycling, and when you consider the likes of Russia (160t) and other central banks were big buyers plus investors around the world that is a big number. In 2015 we are already seeing that demand continue unabated, indeed if anything ramping up with an incredible 61t of gold consumed in China in just the first week of 2015! So where is it all coming from? Historically the biggest ‘vault’ sources are London and New York. Eurostat reported net exports from the UK last year (excluding Dec) of 1,871t so that gives a measure on London. New York is less clear but we had confirmation that the Dutch were successful in repatriating 122t and Germany (despite demanding 300t 2 years ago) still only received a trickle. The $100b elephant in the room however is the Chinese central bank who haven’t told us their inventory since 2009 and not whisper since on purchases. That said the graph below (courtesy of the excellent Tocqueville newsletter we’ve posted for you today) gives a likely insight as their reduced purchase of US Treasuries with cash reserves will almost certainly have been replaced with gold purchases. The Chinese are very clever. They are quietly buying up big time at bargain prices in readiness for the collapse of the current global economic central bank stimulus experiment. Are you?