Wall St Whipsaws - What Next?

News

|

Posted 06/05/2022

|

12076

Last night continued the biggest sharemarket whipsaw since peak COVD turmoil in mid 2020. After the biggest Fed day surge in 44 years on Wednesday night, last night saw the biggest drop since June 2020 with the NASDAQ down 6% at its worst and 5% at close. The S&P500 was down over 3.5% as well and to complete the reversal of ‘all things’ bonds tanked (yields shot up), the other safe haven of gold also fell back below US$1900, and the USD surged to wipe out yesterday’s gains but saw a much weaker AUD and gold hold steady in AUD terms. So what on earth is going on?

With the NFP payrolls due out tonight to finish the week we have already in the last week seen the biggest drop in the S&P500 last Friday since June 2020, then the biggest gain Wednesday night since May 2020, and last night’s carnage as mentioned above. We haven’t seen whipsawing of markets like that since 1985.

As usual of late this seems to be all caused by the market trying to reconcile the growing consensus of longer term high inflation with more signals of economic weakness. Just a week ago the US printed a negative GDP for the last quarter, one quarter away from recession. Last night there was more poor data with US layoffs increasing, rising Jobless claims, poor online retail sales data, and productivity dropping in the first quarter by the most since 1947. Again, stagflation looms large. From Bloomberg:

“Doubts that policy makers can arrest runaway prices rocked markets, with the prospect of stagflation unsettling investors. By pushing back on a jumbo-hike of 75 basis points in June, Fed Chair Jerome Powell beat back traders’ most-aggressive predictions. However, it’s still a bumpy road ahead, with pivotal economic data and global developments that could seed doubts about the central bank’s approach. Friday’s jobs report is expected to show solid payroll growth and wages holding at exceptionally high levels -- remaining an enduring source of inflationary pressures.”

The stickiness of inflation is the key. Last night US Treasuries saw a pronounced bear-steepening with a 30yr UST cycle peak at 3.21%, on concerns the Fed isn’t doing enough to stop inflation while speculation over fund liquidations grows. Remember longer dated bonds largely dictate mortgage rates and the US is now looking at the highest mortgage rates since the GFC in August 2009. How would Aussie home owners fair?

That gold went down last night might seem perplexing to those who understand it. Last night was simplistically an inflation fear trade presenting as higher rates, particularly at the long end of the curve. There is an ingrained misunderstanding that higher rates are bad for gold. As we have written before that is historically completely wrong as the type of rising rates we are seeing are usually ‘too little too late’ and against rising inflation and an inevitable reversal on the indebted system breaking and gold outperforming… every time. Gold sits nicely in the low to negative real rates space, as an inflation hedge and safe haven asset on the inevitable outcome. Markets routinely initially get it wrong before piling in after the smart investors have bought early at lower prices.

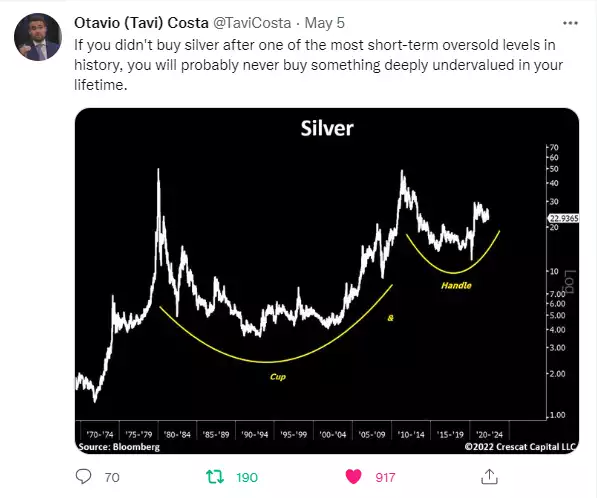

The cup & handle technical setup for gold supports this and the same can be said for silver which the following tweet from Crescat’s Tavi Costa so perfectly illustrates..