Shares at “extreme” overvaluations

News

|

Posted 03/12/2015

|

6453

You’ve got to love these ‘markets’ nowadays… Yesterday we reported on how stocks jumped on bad core economic news – likely because they believed the free money game would continue. Last night we had the opposite where the Fed Chair reiterated their need to start raising rates. Those who read our article on why a rate rise could be good for gold and silver may be amused to know she last night stated that delaying a rate rise could lead to a recession. So on news that the economy is in good enough shape to raise rates, what happens to US stocks? Dow Jones down nearly 159 points! Clearly this is not a market based on fundamentals, it is a casino.

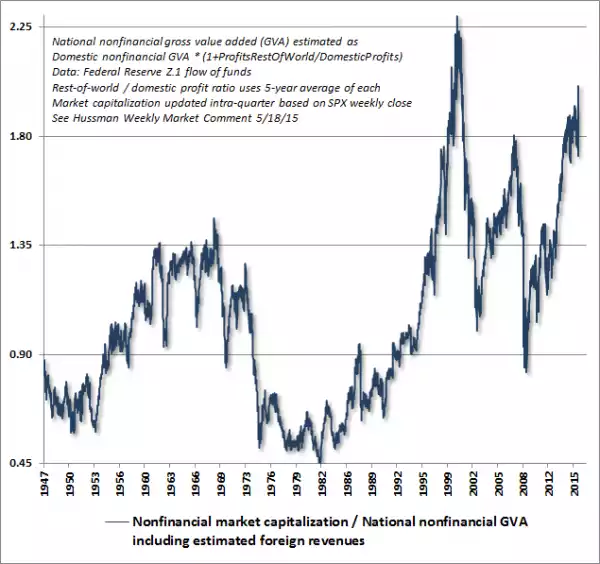

To back this up (and as promised yesterday) financial analyst John Hussman recently looked at what financial metrics or overvaluation measures best predict where a market might go (using the US’s S&P500 as the base ‘market’). Acknowledging that few have strong correlations to short term returns he looked at the ensuing 10-12 year period – a ‘normal’ investment horizon. In terms of correlation the often highly regarded Shiller P/E (price / earnings) index saw an 84.7% correlation. The best was the Non-financial market capitalization / Gross Value Added ratio (MarketCap/GVA) with an impressive 91.9% correlation.

The graph below shows this ratio mapped over the last 50+ years. You can clearly see the current level exceeds all previous busts barring that of 2000 (the extraordinary tech bubble bust). This current level even exceeds the Great Depression bust of 1929 and 1937.

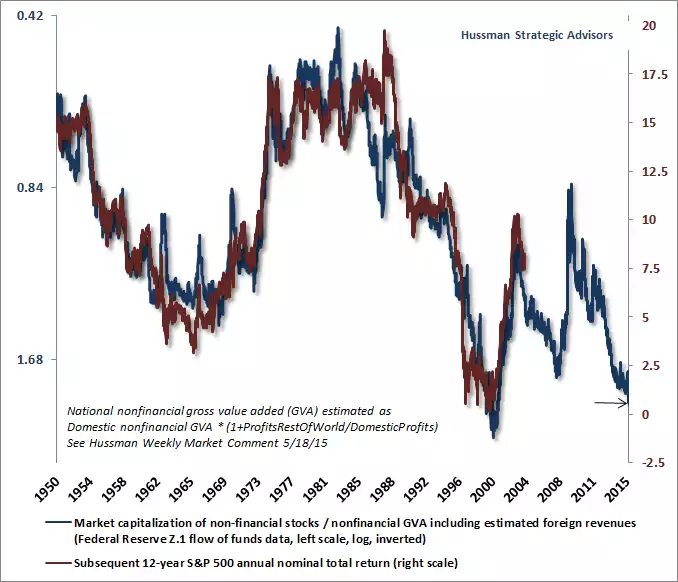

The chart below then inverts that ratio and puts it against the subsequent actual S&P500 returns over the ensuing 12 years (you can see that 91.9% correlation). So, just as the 12 years from just prior to the 2000 crash saw near zero returns, the model is now saying the next 12 should see less than 1% - and that includes dividends!

What this model appears to show is that not only are we way overdue a big correction in the US sharemarket (and we all know if the US sneezes we catch the cold), but those buying in now for ‘yield’ over the long term, unconcerned about capital losses in the interim, may also see next to zero regardless. Or as John Hussman himself said:

“Given both obscene valuations and clearly unfavourable market internals and credit spreads at present, we see extreme market losses as not only an immediate risk, but also as the predominant likelihood over the next few years.”