Now Is the Time to Buy Gold

News

|

Posted 04/02/2014

|

3944

Bud Conrad, Chief Economist

Now Is the Time to Buy Gold

Gold has been in a downturn for more than two years now, resulting in the lowest investor sentiment in many years. Hardcore goldbugs find no explanation in the big picture financial numbers of government deficits and money creation, which should be supportive to gold. I have an explanation for why gold has been down—and why that is about to reverse itself. I'm convinced that now is the best time to invest in gold again.

Gold Is the Alternative to Non-Convertible Paper Money

If you've been a Casey reader for any length of time, you know why gold is a good long-term investment: central banks are expanding paper money to accommodate the deficits of profligate governments—but they can't print gold. Since the beginning of the credit crisis, the world's central banks have "invented" $10 trillion worth of new currencies. They are buying up government debt to drive interest rates down, to keep countries afloat. The best they can do is buy time, however, because creating even more debt does not solve a credit crisis.

Asia Is Accumulating Gold for Good Reason

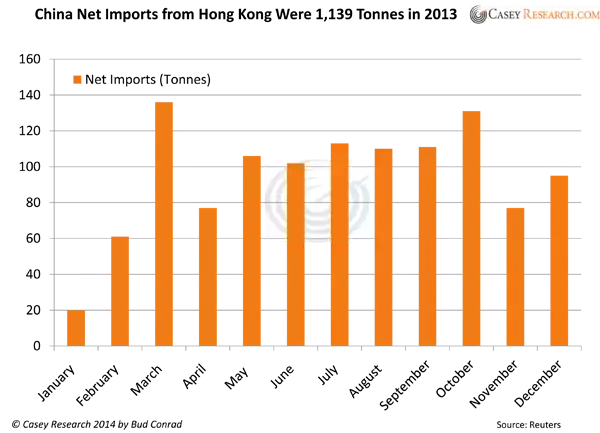

Since 2010, China has been buying gold and not buying US Treasuries. China's plan seems to be to acquire a total of 6,000 tonnes of gold to put its holdings on a par with developed countries and to elevate the international appeal of the renminbi.

In 2013, China imported over 1,000 tonnes of gold through Hong Kong alone, and it's likely that as much gold came through other sources. For example, last year the UK shipped 1,400 tonnes of gold to Swiss refiners to recast London bars into forms appropriate for the Asian market.

China mines around 430 tonnes of gold per year, so the combination could be 2,430 tonnes of gold snatched up by China in 2013, or 85% of world output.

India was expected to import 900 tonnes of gold in 2013, but it may have fallen short because the Indian government has been taxing and restricting imports in a foolish attempt to support its weakening currency. Smugglers are having a field day with the hundred-dollar-per-ounce premiums.

Other central banks around the world are estimated to have bought at least 300 tonnes last year, and investors are buying bullion, coins, and jewelry in record numbers. Where is all that gold coming from?

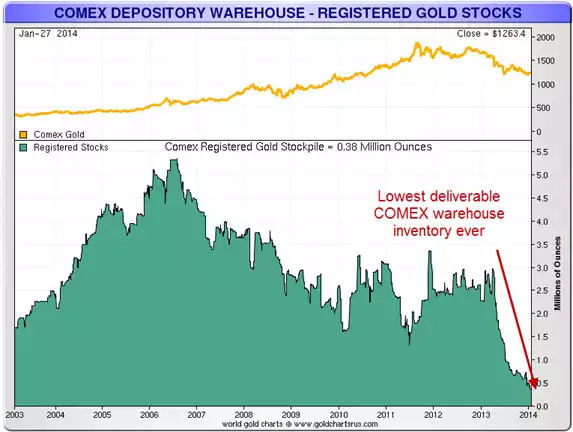

COMEX and GLD ETF Inventories Are Down from the Demand

The COMEX futures market warehouses dropped 4 million ounces (over 100 tonnes) in 2013. The COMEX uses two classes of inventories: the narrower is called "registered" and is available for delivery on the exchange. There are other inventories that are not available for trading but are called "eligible." I don't think it's as easy to get holders of eligible gold to allow for its conversion to registered to meet delivery as the name implies. Yes, that might occur, but only with a big jump in the price.

The chart below shows the record-low supply of registered COMEX gold.

Meanwhile, SPDR Gold Shares (GLD), the largest gold ETF, lost over 800 tonnes of gold to redemptions. At the same time, central banks have provided gold through leasing programs (but figures are not made public).

Why Has Gold Fallen $700 Since 2011?

In our distorted world of debt-ridden governments and demand from Asia, gold should continue rising. What's going on?

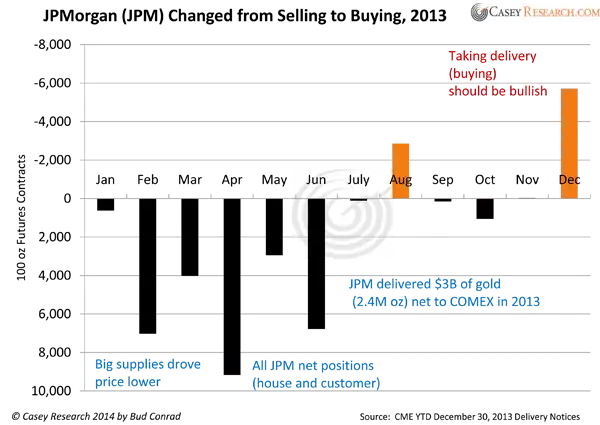

The gold price quoted all day long comes from the futures exchanges. These exchanges provide leverage, so modest amounts can be used to make big profits. Big players can move markets—and the biggest player by far is JPMorgan (JPM).

For the first 11 months of 2013, JPM and its customers delivered 60% of all gold to the COMEX futures market exchange; that, surely, is a dominant position that could affect the market. By supplying so much gold, they are able to keep the price lower than it would otherwise be.

A key question is why a big bank would take positions that could drive gold lower. Answer: Banks gain by borrowing at zero rates. But the Federal Reserve can only continue its large quantitative easing programs that bring rates to zero if gold is not soaring, which would indicate weakness in the dollar and the need to tighten monetary policy. Voilà—we have a motive. Also, suppressing the price of gold supports the dollar as a reserve currency.

The chart below shows the month-by-month number of contracts that were either provided to the exchange or taken from the exchange by JPM. For a single firm, the numbers are large, but the effect across all gold markets is greater because so many gold transactions follow the price set in the paper futures market.

What jumps out from the chart above is the fact that while JPM had been selling gold into the futures market for most of the year, it made a major shift in December, absorbing 96% of all gold delivered.

That is a radical shift and, I believe, an indicator that JPM's policy has shifted. In my opinion, their deliveries of gold were suppressing the price during 2013, but now their policy has shifted in a way that will support gold going forward.

This leaves a vital question unanswered: Why? Has the motivation to suppress the price of gold gone away? Not likely, and we may never know the full truth of what is happening, but I suspect the main reason for the shift is that they have done their damage. The $740 drop from top to bottom, a 39% decline, has shaken confidence in gold as a financial "safe haven" among many investors, especially those new to precious metals. At the same time, continuing to lean on gold at this point could become very costly. JPM delivered $3 billion (about 2 million ounces of gold) into the market up to December in 2013, and may not have ready sources of gold to keep that up. It is dangerous to put on big short positions unless you have gold or some future gold deliveries as a hedge.

By now, everyone knows of the shortages in the gold market; JPM has to be as aware of that as the rest of us. It just isn't safe for them to continue to lean on the market. Being aware, it looks like they are taking the bet that gold will rebound, so they could do well on the other side of the trade.

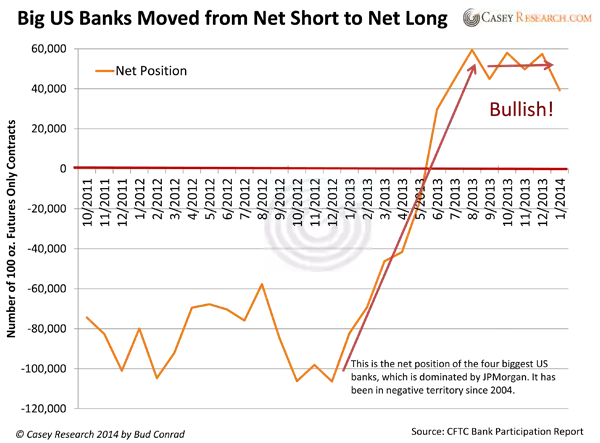

Another confirmation of the shift by big banks comes from data provided by the US Commodity Futures Trading Commission (CFTC) that shows the net positions of the four biggest US banks in the futures market. There has been a dramatic change from being short the market to now being long.

Crisis Brewing in the Gold Market

Germany claims to hold 3,390.6 tonnes of gold, about half of which is held by foreign central banks. Over a year ago, they announced a plan to repatriate 674 tonnes of gold from France and the United States. The US said it would comply, but told the German government that it would have to wait seven years for all the gold to be delivered. The news out last week was that after a year, Germany had only obtained 37 tonnes of its gold—and only five of them were from the US. That is a trivial amount (only 160,000 ounces).

So why can't Germany get its gold? Explanations of having to melt down existing gold and recast it just don't make sense. The most logical conclusion, and the one I've come to, is that the United States simply doesn't have the gold it says it has—neither Germany's nor its own.

Of course, the US government isn't going to admit that there's a problem, but I say there is.

More evidence: JPMorgan's COMEX warehouse contained 3.0 million ounces of gold in 2012, but that had dropped to 0.5 million ounces by mid-2013. Its registered inventories are a razor-thin 87,000 ounces. These kinds of swings are indicative of shortages and instability.

Further, JPMorgan sold its gold vault in New York City—located next to the Federal Reserve's vault—to the Chinese. The banking giant also just announced the sale of its commodities trading business (although it may not have sold the precious metals part of that business). Perhaps they were concerned about new regulations of banks with deposit insurance from the government.

In another relevant development, Deutsche Bank recently surprised the gold community by quitting its position on the committee that sets the London a.m. and p.m. fixings. This came a few weeks after a German regulatory body called BaFin started investigating how these prices were set. BaFin also gave an indication that the process appeared worse than the LIBOR fixing scandal, which resulted in billions in fines.

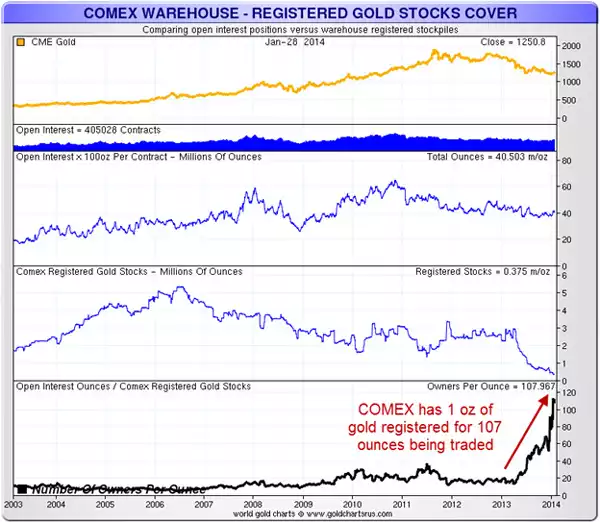

Putting Inventories and Traders Together

The futures market looks fragile to me. The basic problem is that there are many more transactions that could put a claim on gold than there is gold registered for delivery in the COMEX warehouses.

The chart below gives a dramatic picture by simply dividing the open interest of all futures contracts by the registered inventories. The black line at the bottom shows the big jump in the ratio as the registered inventories declined. There are 107 times more open-interest positions than there is registered gold.

The futures markets operate on the expectation that only a few big traders will demand delivery. JPMorgan has shown that it is in a position to demand almost all (96%) of the gold for delivery. They are big enough that they could cause a collapse of the market, if they were to force delivery of more than is available. They know better than to do so, though, and I would guess that they will just manage to try to gain back what gold they have been delivering over the last several years. That should support the price of gold.

Gold Will Rise, and It's on Sale Now

Now is the time to stake your claim in gold. In the long term, we know that paper money will become worthless; in the short term, the biggest seller has just shifted its actions to becoming a buyer. That makes this a good time to accumulate gold and gold mining stocks before a major shift upward in price.