Gold Demand Q1 2018 & Supply

News

|

Posted 11/05/2018

|

8971

Despite gold being up 1% for the year (5% in AUD terms) and the US sharemarket just again breaking even yesterday for the year (and now up a similar amount), gold demand in the first quarter was the worst first quarter in 10 years.

Q1 2018 saw a 7% drop from that of 2017 to 973.5 tonne, largely off weaker investor demand according to World Gold Council’s Gold Demand Trends report for the quarter. The highlights of the report are as follows:

Global bar and coin demand fell 15% to 254.9t

- China*, Germany and the US led the decline. (*see our note below re China)

Gold-backed ETF inflows, softer at 32.4t, were concentrated in US-listed funds

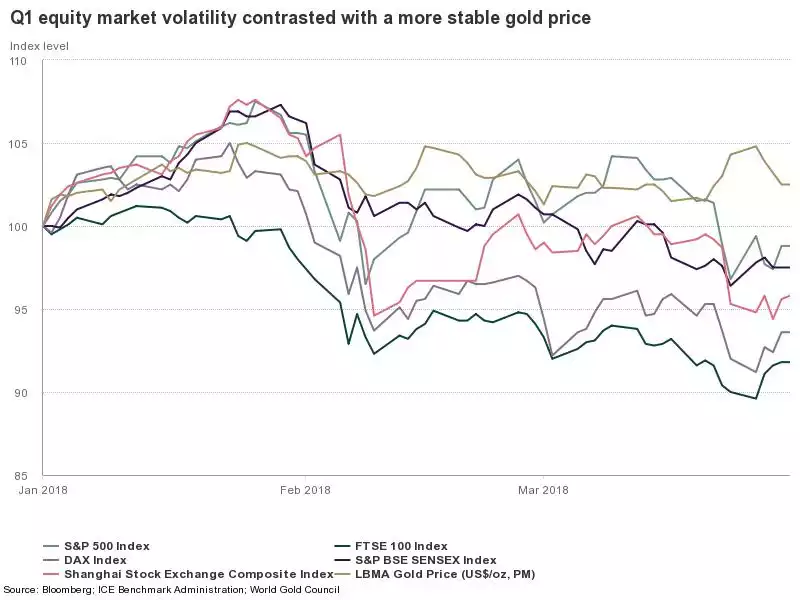

- Whilst softer, it is still the 5th consecutive quarter of inflows into gold ETFs helped by continuing volatility in equities in the US. The graph below illustrates clearly the beauty of an uncorrelated asset like gold as it dances along the top of all the volatility in global equities markets below it:

Central Bank demand rose 42% to 116.5 t

- Highest first quarter since 2014 and continuing an uninterrupted net buying trend averaging 115t per quarter since 2010.

Jewellery demand little changed at 487.7t

- Strength in China and the US offset a weaker quarter in India.

Gold used in the technology sector saw a sixth consecutive quarter of growth

- Up 5% to 65.3 t. The sector saw healthy demand for gold in memory chips and wireless applications particularly off the back of growing use in face recognition in smartphones. Growing 5G upgrades bodes well for future growth.

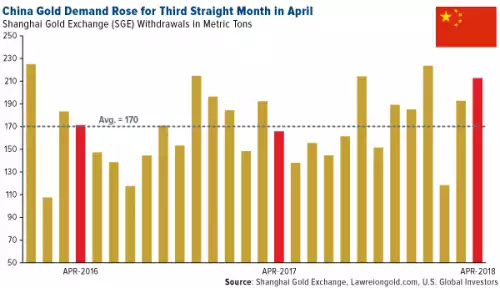

* The continuing disparity between WGC’s China figures and those of outflows from the Shanghai Gold Exchange were evident in this quarter. Many believe the latter is the ‘real’ number whereas the numbers supplied to WGC are deliberately understated. The graph below also shows that despite that very ordinary February in the last quarter, April has kicked Q2 off strongly:

Indian demand was particularly weak with jewellery down 12% and investment down 13%. The quarter was however notable for a lack of ‘auspicious’ gold buying days and the forecasts are for a good monsoon season which should see a reversal of the drought weakness experienced last year.

On the supply side of the equation WGC reported mine supply up 1% to 770 t and recycling unchanged at 287.7 t. We will discuss some broader dynamics in the supply space next week.