Gold & debt

News

|

Posted 24/09/2015

|

7392

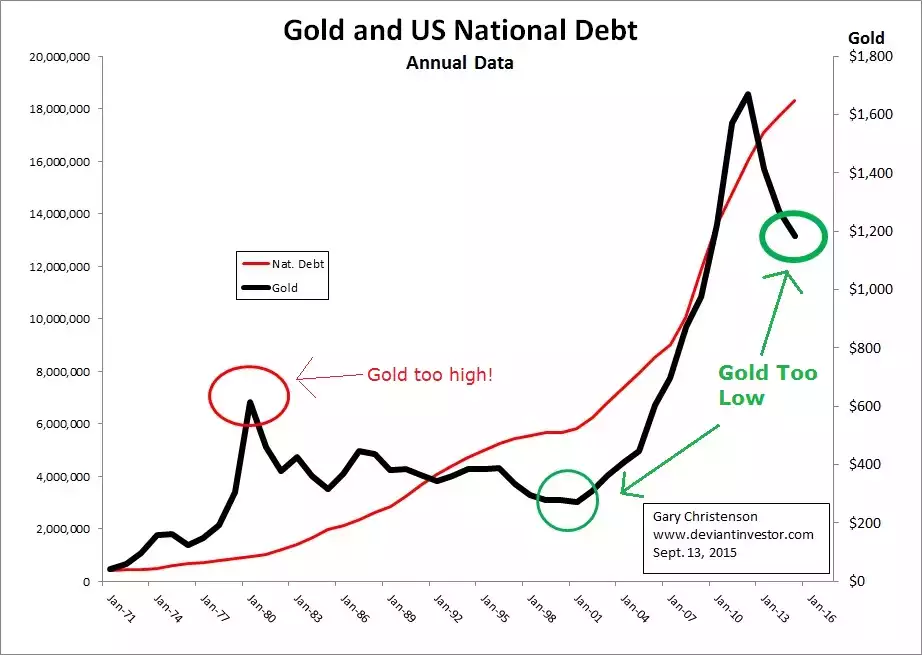

Yesterday saw another 2% fall on our stock market and futures this morning show no sign of a recovery today. With current global stock volatility increasing, it is looking very much like we are ending an era of stock and bond prosperity fuelled by central bank stimulus; itself backed by only credit and faith. It’s timely then that another indicator is also pointing towards a cyclic shift at this time. The following graphs plot the gold price in US dollars along with the US national debt and it is evident that the former tends to track the latter within the range of a price channel. At some points in history, the gold price tends to overshoot the debt level and at other times it undershoots but there is a definitive correlation.

If we look at gold pricing from January 1996 to July 1999 we see a drop from about $405 to $253 representing a 38% downward movement in a time span of 42 months. This period of time was an example of a “debt undershoot” and is interesting as it preceded the decade long rally to $1900 achieved in August 2011, a point where the gold price had overshot the debt level at the time. From that point, we again see a retracement in the gold price to $1070 in July 2015 representing a 44% drop in 47 months; a move very reminiscent of the 1996-1999 collapse.

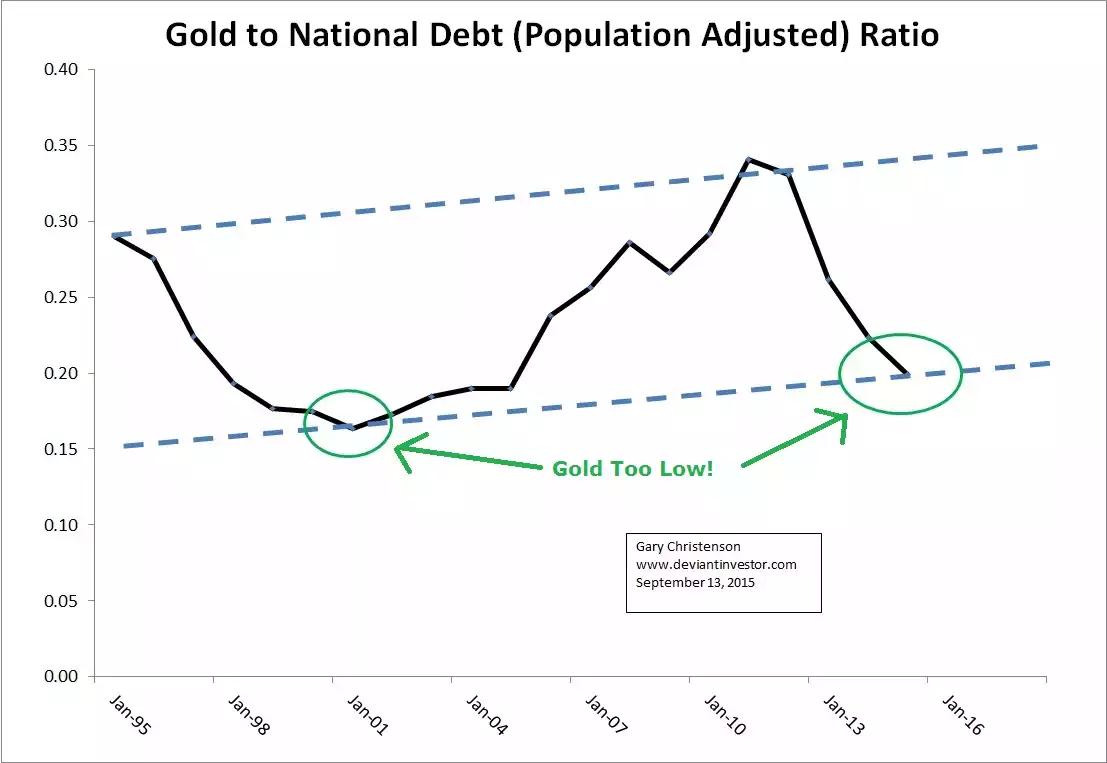

As the green circles in the graphs above and below indicate, currently we are at a historically low gold to debt level (another “debt undershoot”) and this would indicate significant upside potential at this time. The second chart below illustrates how the gold to debt ratio on a population adjusted basis has behaved within a price channel over the 20 year time period described above. Again, it is clear that gold prices rise with debt and that current pricing is at the lower bound of a multi-decade range. Another way to think about this is to consider that the last 4 years of price declines have built up an imbalance which needs to be corrected as it was in 1999.

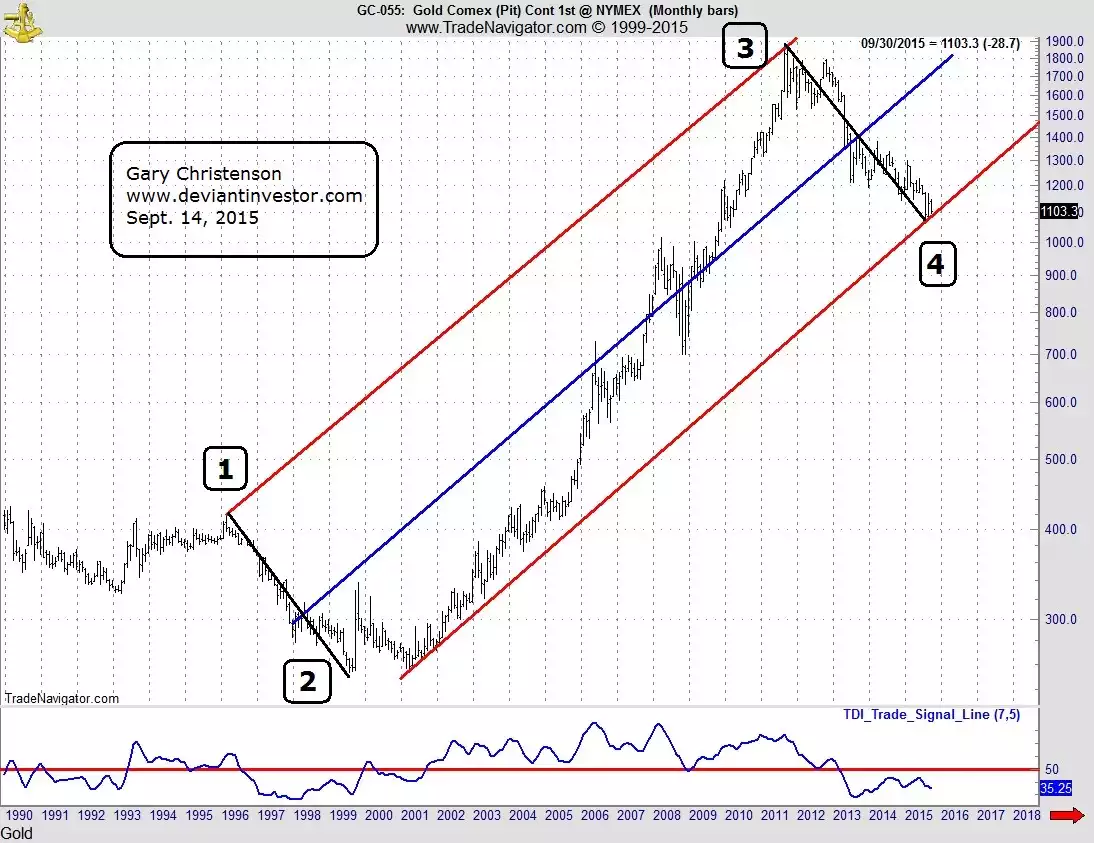

Lastly, the following plot of the gold price highlights the significance of today’s price level as labelled by point number 4. It matches the lower bounds of the price channel trajectory which extends from the end of the previous gold bear market labelled by point number 2. With the historical evidence of this gold price channel established, it is completely reasonable to assume that as national debt increases, gold prices consequently have considerable upside and that is without considering the potential risks of hyperinflation or a currency panic.