From QE to QT – The US Fed’s next big move

News

|

Posted 26/06/2017

|

8916

Our views on the world’s central banks looking to tighten into such a weak economy are well known. Last week James Rickards (via The Daily Reckoning) warned for us to get ready for QT1 – Quantitative Tightening as opposed to QE – Quantitative Easing. This is the process we discussed last week of reducing the $4.5 trillion of bonds it bought with freshly printed money during QE, whilst also raising rates.

“The Fed hiked rates not because it believes the economy is getting stronger, but because it is desperately trying to catch up — before the next crisis. [allowing them to cut rates and buy bonds to try and save the economy, as they currently have no ammunition to do so].

They are now trying to normalize the balance sheet. Under the Taylor Rule a normal balance sheet at the current expansion rate could be expected to be at $2.5 trillion. That means you have to take $2 trillion of money and make it disappear.

They can do that by selling securities, but the Fed believes that the market’s too fragile. Instead they’re going to leave securities on the balance sheet and allow them to mature. Think of this as the Fed putting QE in reverse.

The Fed has been rolling over the balance sheet to keep it at $4.5 trillion.

You’ll be hearing more about quantitative tightening in the weeks and months ahead for 2017.

What quantitative tightening means is that they’re going to stop rolling it over.

That means as securities mature and the Treasury sends out money they’re not going to buy, replenish or buy more. This should cause the balance sheet to shrink and the money supply to be reduced. The Fed is not going to do it all at once.”

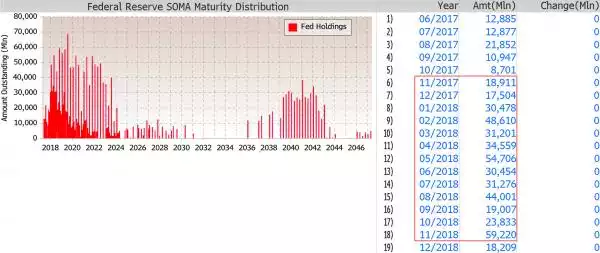

For newcomers this simply means that when you buy a US Treasury bond (with your money created out of thin air if you’re the Fed), it has a duration or expiry. At the end of that period the issuer (US Treasury) gives your principal back unless you ‘roll it over’ which means keep it and renew for another term. So rather than the US Fed selling its $4.5t hoard of bonds, it will just let them mature and hence reduce its balance sheet. That looks a little like this:

As you can see the majority mature over the next 7 years, hence the ‘all at once’ remark above. The big question however is how long do they have before they need to (re)loosen, not tighten their policy…. Over to Mr Rickards…

“By raising rates and leaving open the possibility of further increases, all of the monetary actions being taken are tightening the economy. The Fed’s QT policy that aims to tighten monetary conditions, reduce the money supply and increase interest rates will cause the economy to hit a wall.

The decision by the Fed to not purchase new bonds will be just as detrimental to tightening of the economy as raising interest rates.

The economy is slowing. Even without any action, retail sales, real incomes, auto sales and even labor force participation are all declining. Every important economic indicator shows that the US economy is slowing right now. When you add in rate hikes and QT, we may very well be in a recession by later this year.

The Fed is tightening into weakness.

Because they’re getting ready for a potential recession where they’ll have to cut yet again. Then it’s back to QE. You could call that QE4 or QE1 part 2.

The point is that the Fed has essentially trapped itself into a state of perpetual manipulation.”

“Now is the time to increase your allocations to cash, gold, silver and U.S. Treasuries.

Preparing now will offer the best insurance position in the wake of the coming crash.”

But don’t just take James Rickards word.. the central banks’ central bank, the Bank of International Settlements (BIS) just had this to say in their annual report:

“Policy tightening to contain an inflation spurt could trigger, or amplify, a financial bust in the more vulnerable countries. This would be especially true if higher policy rates coincided with a snapback in bond yields and US dollar appreciation: the strong post-crisis expansion of dollar-denominated debt has raised vulnerabilities, particularly in some emerging market economies (EMEs).”