Fed Hikes, Libor Spikes & Gold Likes

News

|

Posted 22/03/2018

|

9663

New Fed Chair Jerome Powell resided over his first FOMC meeting last night where the Fed raised rates by 0.25% to 1.75%. Powell talked up the economic recovery, clearly looking past the softness of this last quarter and whilst the committee was unanimous on this hike, it was split on whether it would be 4 or 3 hikes this year. Market consensus appears to be for 3 hikes in 2018, 3 in 2019 and 2 in 2020.

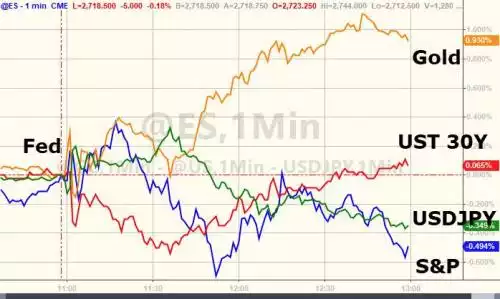

The market reaction was shares down, bonds up, USD down and gold and silver up as there are very clear concerns about the effects of the free money game coming to an end, how the market will survive without it and how all that debt will be serviced with higher rates.

Whilst gold and silver rose strongly in USD spot terms, up $24 and 44c respectively, surprisingly the AUD rallied 1% effectively halving those gains in our local currency. We say ‘surprisingly’ as this is the first time the Aussie interest rate (1.5%) has been less than the US (now 1.75%) in a very long time, and last time saw an AUD of around US50c. That would raise the question of why money would buy AUD over USD and hence actually go up (78c) not down? Is this a faith in USD issue or a short term phenomenon? Either scenario could be extraordinarily bullish for Aussie gold holders.

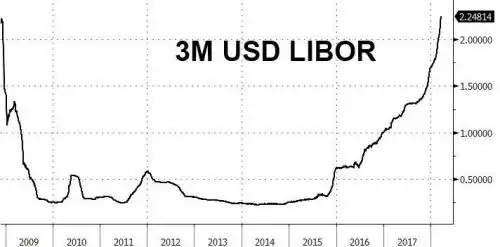

But as we wrote last week, despite these moves in the ‘public’ interest rates, the private market is sending a very clear, and very concerning signal. When we wrote about the spread between the Libor (benchmark credit rate) and OIS (the ‘risk free’ rate) it was at its highest since the Euro debt crisis of 2012. Last night it widened to 55.6bps, the biggest gap since the GFC.

Additionally in a pure Libor rates sense (not the risk spread) the graph below shows again we are at rates not experienced since the GFC, and rising sharply:

Citibank’s Matt King explained yesterday why that matters:

“LIBOR is still the reference point for the majority of leveraged loans, interest-rate swaps and some mortgages. In addition to that direct effect, higher money market rates and weakness in risk assets are the two conditions most likely to contribute towards mutual fund outflows. If those in turn created a further sell-off in markets, the negative impact on the economy through wealth effects could be greater even than the direct effect from interest rates.”

Reinforcing this view Morgan Stanley’s Chief Strategist chimed in saying:

"That’s a key reason why markets have struggled. The acceleration in the private borrowing market [Libor] is the story of the year, not the Fed," and "this sets us up for a market which we are pretty sure reached its highs for the year in the euphoria of the third week of January and the rest of the year is quite simply going to be a tough market."

Markets falling last night and gold surging would suggest he is not alone in his thinking, and the Fed just reinforced the trajectory…