Earnings Flag More Pain to Come

News

|

Posted 29/06/2022

|

14068

Another shocker on Wall Street last night with heavy falls across the board. The only thing positive was the USD and some commodities, and gold was pretty much flat but up in AUD terms. So what happened this time?

The route was triggered mainly by US Consumer Sentiment missing market expectations of 100 and printing a 16 month low of 98.7, down from 103.2 last month. The survey also paints a grim picture looking forward with the survey starting: “Expectations have now fallen well below a reading of 80, suggesting weaker growth in the second half of 2022 as well as growing risk of recession by yearend.”

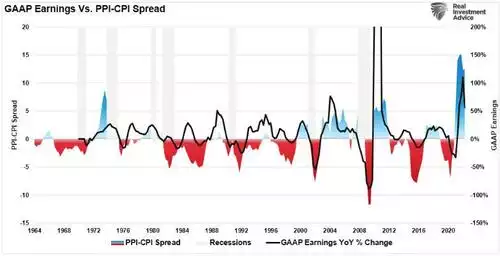

The key concern of course was again inflation. The problem remains that the combination of high inflation and a weak economy, stagflation, is not a good one. Businesses already struggling with margin squeeze, unable to pass on their rising input or wholesale costs, will continue to see earnings pressures which continues to put pressure on their share price now that the market is actually seemingly assessing price earning valuations like a normal market does… Exhibit A below clearly shows the extent of this squeeze..

The author of that chart, REA’s Lance Roberts rightly points out:

“Notably, while forward P/E ratios have declined, much of that is due to the decline in the “P” and not the “E.” Therefore, if an earnings recession is coming, as the data suggests, then the current “bear market” cycle still has more work to do.

The realignment of market prices and valuations is always a brutal process. While many believed the Fed had eliminated bear markets and economic recessions, the business cycle can only be delayed but never repealed.”

Goldman Sachs issued the following warning yesterday as well:

"If our model proves to be correct, we may see large cuts to earnings ahead. Assuming no change in expected revenues, margin compression alone could reduce the median stock's expected 2023 EPS growth from +10% to 0%."

Last week Nicholas Colas of DataTrek Research discussed the implications from an index pricing perspective for the S&P500 (the index was 3667 compared to 3821 now after the relief rally last week):

“Pulling this discussion into the present day, all we know for sure is that equity markets don’t believe S&P 500 earnings will grow over the near term from their recent run rate of $54/share ($216/year). With the index’s close of 3,667 today, we are trading at 17.0x current earnings. That’s a fair multiple, spot on the 10-year average. This implies the market believes incremental revenues and margins (operating leverage) net to zero percent growth over the next year.

The history of earnings during recessions can give us a sense of where US large caps might bottom. Here are 3 scenarios, each using the same 18x multiple, not the 17x long-run average, for trough earnings since markets will assume strong incremental earnings leverage off the bottom for the reasons described earlier.

- Modest earnings decline (15 percent): $184/share (down from $216/share currently)

- Earnings go back to 2018 – 2019 levels: $162/share, -25 percent

- Typical recessionary earnings decline (28 percent, average of 1990 and 2000 – 2002); $155/share

They are big further falls for a market already down over 30%.

Nick Hubble yesterday talked to the ‘Everything Bubble’ created by unprecedented central bank stimulus that saw everything go up, and for shares fundamentals like Price Earnings go out the window. He concludes as follows:

“But what goes up on a wave of central bank stimulus must come down, regardless of inflation and a bear market. As the economist Ludwig von Mises explained, it’s only a matter of time and severity:

‘There is no means of avoiding the final collapse of a boom brought about by credit expansion. The alternative is only whether the crisis should come sooner as the result of voluntary abandonment of further credit expansion, or later as a final and total catastrophe of the currency system involved.’

Japan is currently testing the theory.

In simple English, central bankers pumped up the market to such highs that they must all fall now that central bank stimulus is being withdrawn.

Previously such price action – the boom and the bust – applied to isolated sectors of the market like property in 2006, tech stocks in 1999, Asian stocks in 1996 and so on. But this time, we’re in the Everything Bubble: the central bankers had pumped up everything. And so, everything must come down together, whatever the economic and financial conditions might be.

Another explanation is that the combination a recession and inflation is a rare one which is bad for all asset classes. Remember, inflation and recession are supposed to be mutually exclusive.

Economists simply presumed this to be the case until the 1970s.

Investments which rely on a hot economy are falling because of a recession and investments which rely on low inflation are falling as prices surge.

The thing is, both measures are yet to get a lot worse. The Bank of England’s latest forecast is for inflation to top 11%. And a recession is only just emerging as a consensus forecast.

The market rout may be only the beginning.”

Whilst gold may be ‘boring’ lately as it dances either side of US$1850, it stands alone as an asset that has held strong and historically the setup is for it to continue to do so and indeed rise on such a reset.