Collapsing Yield Curve Portends Trouble Ahead

News

|

Posted 20/04/2018

|

8722

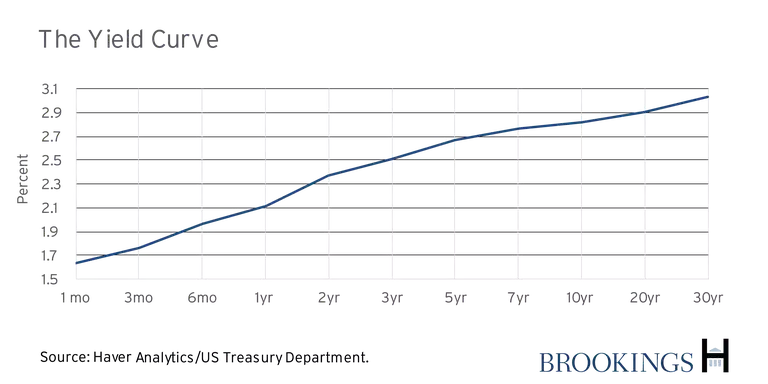

Despite a bounce back yesterday, there is growing talk and concern around the flattening of the US Treasury yield curve. We discussed and explained this previously here, but in essence it is the plot of the yields of varying maturity US Treasury debt and a couple of days ago looked like this:

What everyone is focussing on is the spread between the maturities. The smaller the spread the flatter the curve. The following chart shows the various spreads of 2&30 year, 10&30 year and 2&10 year as a good range (note the pink areas are recessions):

It is the precipitous nature of the collective falls, particularly since the March Fed rate hike, that has markets on edge with all spreads now at lows not seen since just prior to the GFC. What everyone fears is an ‘inversion’ where they dip below zero, something you can see is getting very close. Per that previous article we wrote “That has happened only 8 times since 1958 and in 6 of those occasions was followed by a recession.”

It is certainly worrying members of the US Fed too as continuing to hikes rates into such an environment would be incredibly dangerous. Just this week San Francisco Fed President John Williams warned that he would view "yield curve inversion as warning signal" and that an "inverted curve was a powerful recession signal" and "if the yield curve inverted, her would take it seriously.". That was reinforced with St Louis Fed President James Bullard stating this needed to be debated by the FOMC right now predicting it could invert within 6 months. The Fed of course has not always heeded such warnings. From Bloomberg:

““A potential curve inversion should be taken as seriously as always,” Citigroup analysts led by Jabaz Mathai wrote in an April 13 report. “The historical relationship between the curve and implied recession probabilities is highly non-linear: implied probabilities grow very fast when the curve moves into inverted territory.”

In the report, Mathai argued that the Fed is wrong on the yield curve, again. He noted that in 2006, then-Chairman Ben S. Bernanke said he didn’t see inversion as portending an economic slowdown.”