Central Banks Dump US Treasuries

News

|

Posted 09/10/2015

|

4790

We have covered on a number of occasions the issue of China’s sale of US Treasuries with particular reference to SDR consideration. We’ve also discussed in recent times how the sale of US debt features in the context of funding China’s ongoing gold acquisition project. One may be forgiven for thinking then that the liquidation of USTs is superficially a phenomenon uniquely relevant to China. In reality however, the US$12.8 trillion Treasury market is seeing its biggest selloff in history.

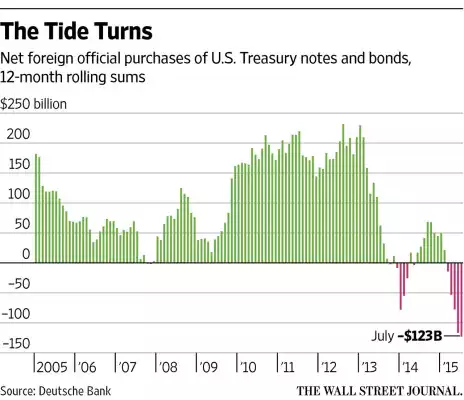

In what seems to be at least partially a consequence of the slowdown in emerging markets, nations that previously were significant acquirers of US debt such as China (as we’ve already mentioned), Taiwan, Brazil and Russia are now selling as the chart below illustrates.

What’s alarming is how quickly this trend has arisen. To provide some context, last year central banks purchased US$27B of US debt yet according to Deutsche Bank, data ending at July this year shows a 12 month liquidation totalling US$123B. The circumstances that supported the former purchases included healthy emerging market trade surpluses that allowed the bolstering of foreign exchange reserves and many opted for the seemingly liquid and safe USD. There are many conclusions one can draw from this year’s trend including a reduction in the faith of the reserve currency, reaction to declining commodity prices and a necessity to support local currencies.

According to the Wall Street Journal, “sales by foreign central banks could accompany a further decline in bond yields, by underscoring the depth of economic problems hitting emerging regions” and there is certainly evidence to support such problems. In addition to China, Russia has reduced its UST holdings by almost US$33B for the 12 months ending in July; as did Taiwan with a near US$7B reduction. With particular reference to the degradation in oil prices, Norway has reacted with a reduction of just over US$18B over the same time period.

We have been commonly remarking about the surprising number of metrics that have degraded to GFC record levels but this activity in the UST market represents the most significant since data started in 1978. For all but the most risk tolerant investors, it represents yet another warning bell in the existing chorus and supports strongly the idea of balancing wealth with hard assets.