“What were you thinking?” – Dotcom warning redux

News

|

Posted 09/09/2021

|

9838

The US sharemarket jitters extended last night and is set to see losses in our local market this morning. Whilst some of the pressure was due to weakening growth concerns and worsening COVID fears, paradoxically concerns of tightening supply chains and labour markets yet again raises the dual spectre of forcing the Fed’s hand at tapering amid lurking stagflation. As Bloomberg noted:

“U.S. equities retreated as investors reassessed valuations in light of global economic risks including the spread of the Covid-19 delta variant and reductions in central bank stimulus.”

“Wednesday’s declines came as money managers from Morgan Stanley to Citigroup have turned cautious on U.S. equities. Many investors have begun to see relative U.S. valuations as excessive even as growth elsewhere suffers from renewed Covid lockdowns and travel curbs. They doubt the world is ready for an eventual tapering of central-bank stimulus even as inflation accelerates due to supply shocks. End-of-year seasonality and valuation concerns are adding to the gloomy mood.”

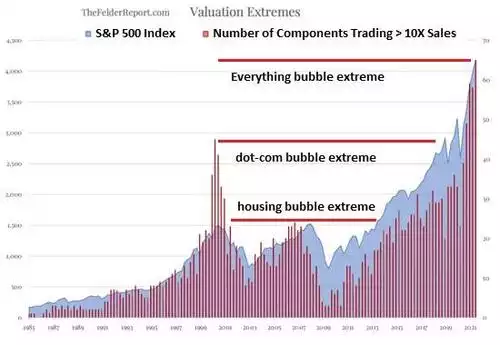

As a reminder of the scale of the “excessive” valuations, just digest that below of S&P500 (in blue) and the number of companies trading in excess of 10 times sales…

So what does 10x Price to Sales mean and are ‘tech stocks’ sitting outside such measures as some argue? The following is from a 1999 Bloomberg interview with Scott McNealy, then CEO of Sun Microsystems, explaining what investors paying 10x Price-to-Sales for his company meant.

“At 10-times revenues, to give you a 10-year payback, I must pay you 100% of revenues for 10-straight years in dividends.

That assumes I can get that by my shareholders. It also assumes I have zero cost of goods sold, which is very hard for a computer company.

That assumes zero expenses, which is hard with 39,000 employees. That assumes I pay no taxes, which is very hard. And that expects you pay no taxes on your dividends, which is kind of illegal.

And that assumes with zero R&D for the next 10-years, I can maintain the current revenue run rate.

Now, having done that, would any of you like to buy my stock at $64? Do you realize how ridiculous those underlying assumptions are?

You don’t need any transparency. You don’t need any footnotes.

What were you thinking?”

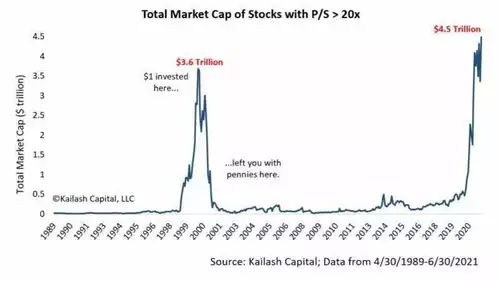

Indeed. Oh, and if you think 10x is bad… below shows there is nearly $4.5 trillion of market cap above 20x!! That is nearly $1 trillion more than the height of the dot com bubble…

The other thing spooking markets last night was the release of the Fed’s so called ‘Beige Book’ being its report on the general US economy. The last report spoke up a strengthening economy, whereas yesterday’s revealed "economic growth downshifted slightly to a moderate pace". The last report was concerned about surging prices and the language softened only slightly to inflation being “steady at an elevated pace” but warned “there continued to be widespread concern about ongoing supply disruptions and resource shortages.”. i.e. slowing growth and sustained high inflation = stagflation. At a time of record high valuations…

In terms of the aforementioned “resource shortages” last night also saw the latest employment data out of the US via the JOLTS report (Job Openings and Labor Turnover Survey). That print surprised to the upside with 10.934m new job openings (against expectations of 10m). With 8.384m ‘unemployed’ that means there are 2.2m more jobs openings than unemployed workers. The market rightly saw that too as inflationary. The only caveat is many of those unemployed are enjoying the COVID emergency dole and that all ends this week…

And so the prospect of the ‘juice’ being tapered from the ‘junky’ is looking more likely and the junky is getting scared. At such addiction levels, rightly so.