“Quantitative Peopling” - Australia’s QE

News

|

Posted 27/11/2019

|

18816

“Quantitative Peopling” - Australia’s QE

The effects of QE around the world are well documented and often spoken about in this forum. As we reported here there is now a growing expectation that Australia’s RBA will join the QE ‘unconventional monetary policy’ game next year.

Today we discovered a very interesting proposition by Macro Business’s Chief Strategist David Llewellyn-Smith that lays out Australia’s own version of Quantitative Easing, what he calls Quantitative Peopling (QP). From his article:

“Let’s consider what QE has done elsewhere:

- by printing money to buy various financial assets, central banks have kept capital constrained banks on life support;

- but that has increased inequality as asset inflation becomes the only game in town for economic gains;

- the result is chronically low interest rates leading to corporations investing in their own shares instead of efficiency or new capacity, as zombie businesses flourish and oversupply is supported endlessly, again entrenching deflation;

- as political dysfunction rises around weak wages and falling real living standards for workers, reform becomes impossible relying ever more upon QE.

That’s your QE feedback loop of doom. QP operates similarly only worse:

- by importing people the government ensures capital constrained banks are supported by artificial demand;

- asset prices like house prices rise and become the only game in town for economic gains;

- but these gains are more than offset by falling wage growth as the labour supply shock crushes worker pricing power;

- universities get ever dumber to attract unskilled third world migrants, locking in low productivity and weak wages;

- the result is chronically low interest rates leading to corporations investing in their own shares instead of either efficiency or new capacity, as zombie businesses flourish and oversupply is supported endlessly, again entrenching deflation;

- all arms of government have to lie in defence of the indefensible as political dysfunction rises around weak wages and falling real living standards for workers, thus reform becomes impossible relying ever more upon QP.

Ironically, the end result of QP is QE, which we will see next year in Australia as we run out of rate cuts. This raises the spectre that we will accelerate all of the negative effects of both policies.”

There are a couple of key points in here that investors should be mindful of.

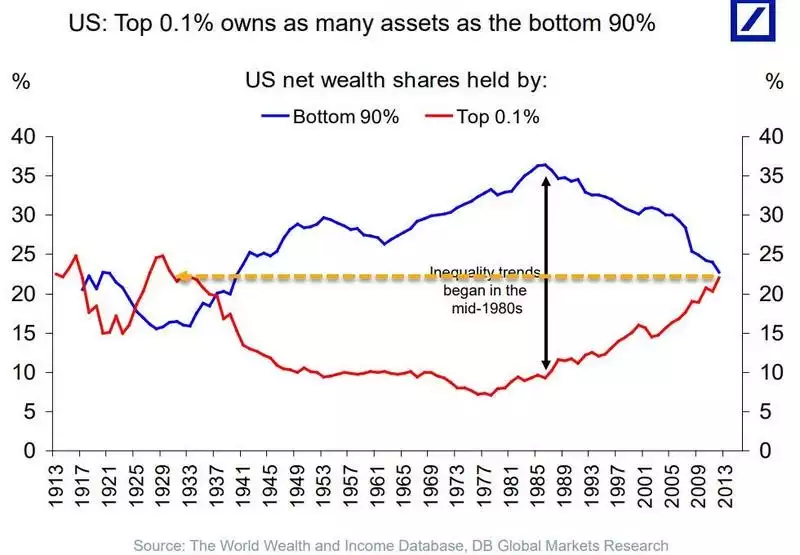

- Both QP to date and QE to come principally drive up asset prices; assets largely owned by the top 10% of the population. Indeed the US have just reached a point in this inequality not seen since just before the Great Depression.

Whilst you might think ‘that’s wrong but what has it to do with my portfolio’, you will recall in our recent article that Deutsche Bank actually put “Continued increase in wealth inequality, income inequality and health care inequality” as their highest ranking risk to financial markets in 2020.

- The fact that most of the stimulus of QP has inflated our housing market speaks again to the risks in the Aussie housing bubble reliant on increased demand through immigration and cheap interest rates.The stagnant wage growth again puts owning a house out of reach of a growing majority of Australians and hence they have not enjoyed the growth in price of this asset class.

The clear alternative for investors looking to ‘keep up’ with the 1% is gold. Like property, gold is a hard asset. Like property gold has enjoyed strong price growth this century. Property has been inflated by QP and possibly further by near zero rates and QE next year. Gold has risen off the back of smart money and central bank demand seeing that this free money party will end badly and preparing themselves. Property has a median entry price of over $500,000. Gold has an entry price of $89 for a 1 gram bar or 1c for Gold Standard tokens (AUS). Property is widely regarded as being ‘at the top’ or ‘in a bubble’ whereas gold is widely regarded as ‘coming off the bottom’.

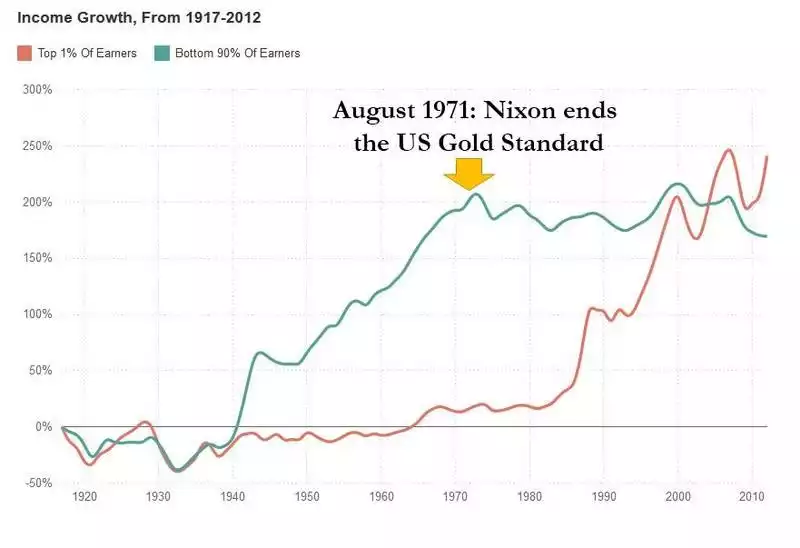

In other words, the greatest asset available to absolutely anyone on any budget to protect their wealth, and indeed profit from this unprecedented credit expansion cycle is arguably the one often thought of as ‘out of reach’ for anyone but the rich. The following chart speaks volumes about the journey since this credit cycle started when we left the gold standard in 1973:

An ounce of gold bought in 1971 cost $44. You may no longer have a currency backed by and protected by gold, but you can easily own the real thing.