“Next Financial Crisis” – Must Read

News

|

Posted 21/09/2017

|

9470

A bit of a break from our usual self penned short and sweet article, but only because we think this is so insightful and credentialed that it deserves to come to you unedited. It’s a clear warning to have uncorrelated monetary assets like gold and silver in your portfolio. It’s from a report the “Next Financial Crisis” by Deutsche Bank’s credit strategist Jim Reid.

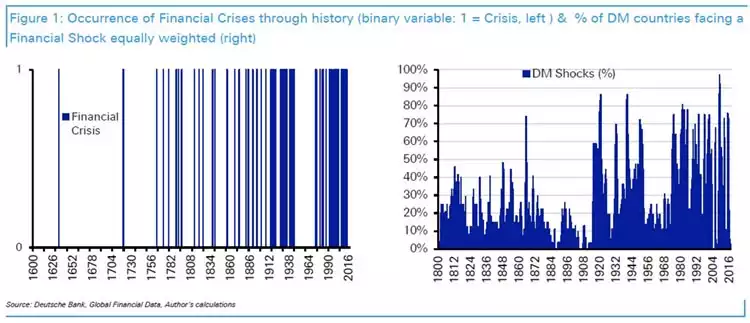

“We think that the post Bretton Woods (1971-) global financial system remains vulnerable to financial crises. A simple internet search of financial crises through history (Figure 1, LHS chart) confirms that the frequency has increased over this period. Examples include the UK secondary banking crisis (1975), the two Oil shocks (1970s), numerous EM defaults (mid-1980s), US Savings and Loans mass failures (late 80s/early 90s), various Nordic financial crises (late 80s), Japanese stock bubble bursting (1990-), various ERM shocks/devaluations (1992), the Mexican Tequila crisis (1994), the Asian crisis (1997), the Russian & LTCM crisis (1998), the Dot.com crash (2000), the various accounting scandals (02/03), the GFC (08/09) and the Euro Sovereign crisis (10-12).

A more quantitative search backs this up (Figure 1, RH chart). We show the number of DM countries (%) in our sample back to 1800 experiencing one of the following on a YoY basis; -15% Equities, -10% FX, -10% Bond move, a sovereign default, or +10% inflation. This is our crisis/shock indicator. 0% equals no country with one of these conditions met, 100% equals all in our sample with one being met.

It would therefore take a huge leap of faith to say that crises won’t continue to be a regular feature of the current financial system that has been in place since the early 1970s. The near exponential growth of finance and its liberalisation since this point has encouraged this trend.

Indeed as we’ll show in this report there are a number of areas of the global financial system that look at extreme levels. This includes valuations in many asset classes, the incredibly unique size of central bank balance sheets, debt levels, multi-century all-time lows in interest rates and even the level of potentially game changing populist political support around the globe. If there is a crisis relatively soon (within the next 2-3 years), it would be hard to look at these variables and say that there was no way of spotting them.

Having said that, crises tend to have a large element of unpredictability. If they didn’t then surely more would predict their imminent arrival. So while we highlight a lot of the main global vulnerabilities in this report, history would tell us that there is still a chance that when the next crisis comes its origin will take us by surprise to a certain degree. As will its timing. In the remainder of this executive summary we highlight the conditions that have encouraged crises through history and the main areas of worry as to why we may be vulnerable for another financial crisis relatively soon.

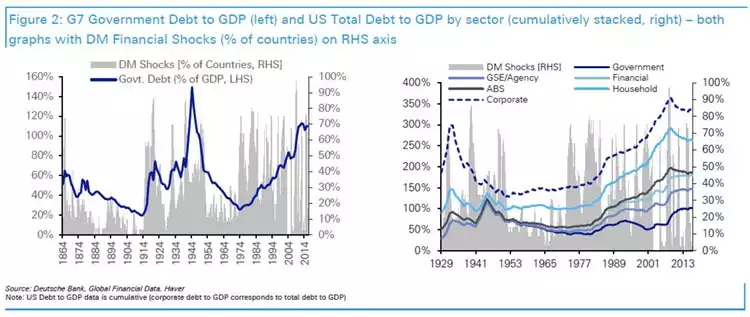

Periods with a higher number of crises/shocks coincide with higher levels of debt….

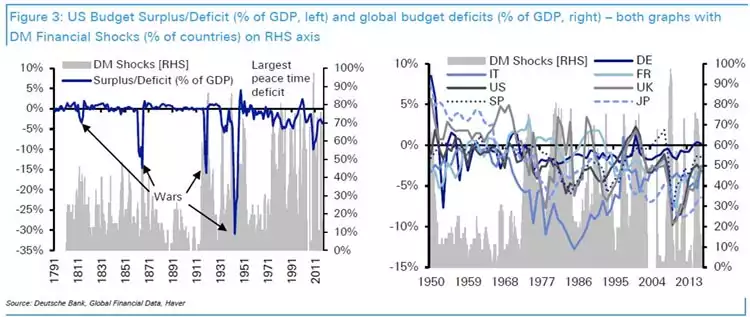

…and with it higher budget deficits. G7 Government Debt was only previously higher with impact of WWII and before the early 1970s, persistent budget deficits only really existed in war time. Now a permanent feature.

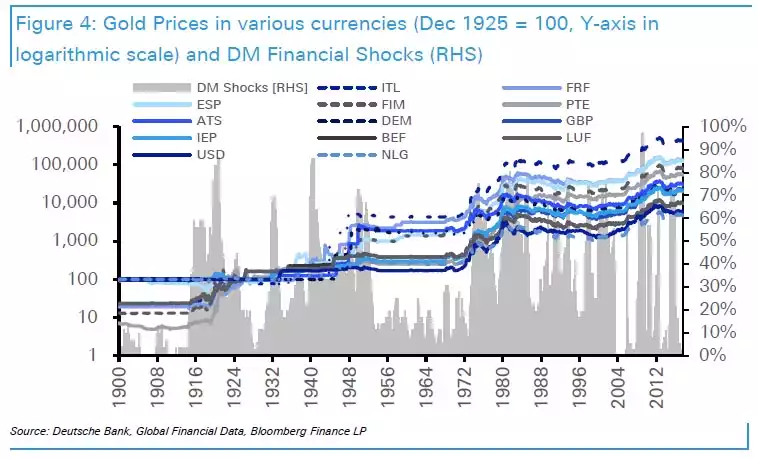

We think the final break with precious metal currency systems from the early 1970s (after centuries of adhering to such regimes) and to a fiat currency world has encouraged budget deficits, rising debts, huge credit creation, ultra loose monetary policy, global build-up of imbalances, financial deregulation and more unstable markets.

The various breaks with gold based currencies over the last century or so has correlated well with our financial shocks/crises indicator. It shows that you are more likely to see crises/shocks when we break from hard currency systems. Some of the devaluation to Gold has been mindboggling over the last 100 years.

Perversely, the current post Bretton Woods system also allows for huge operations/stimulus to overcome any crisis/shock. We also shouldn’t underestimate the positive impact that this can have on nominal asset prices. Cash is arguably a far more dangerous asset in a fiat currency but unstable regime than it is in a more stable less crisis prone one. However, by continually using stimulus to deal with crises and not letting creative destruction take over, you make a subsequent crisis more likely by passing the problem along to some other part of the global financial system, and usually in bigger size. In a fiat currency world, intervention and money creation is the path of least resistance. In a Gold standard world, mining new gold was the only stable way of increasing the money supply.

We think this leaves the current global economy particularly prone to a cycle of booms, busts, heavy intervention, recovery and the cycle starting again. There is no natural point where a purge of the excesses is forced by a restriction on credit creation.

So we’re quite confident that there will likely be another financial crisis/shock pretty soon with their frequency continuing to be high until we create a more stable global financial framework.

So where will the next crisis come from?

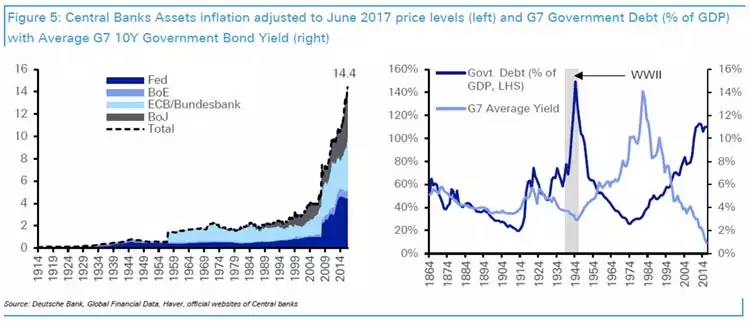

An obvious issue is how we resolve the combination of the unwinding of unparalleled central bank balance sheet sizes at a time of record peacetime government debt and multi-century record low yields (Figure 5).

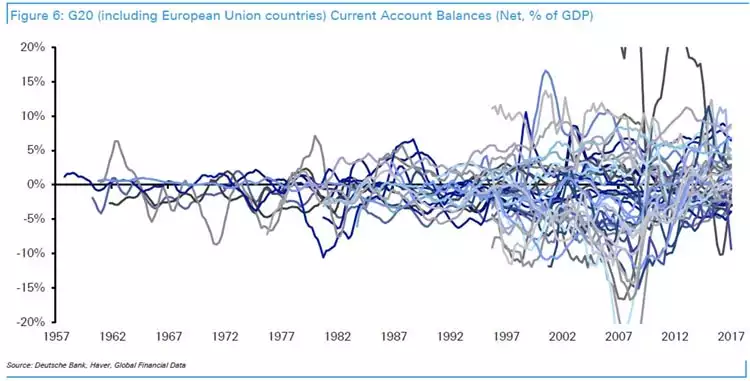

We also still have extreme levels of global imbalances (Figure 6) which pose a risk as international capital flows are necessary to support the status quo. These are harder to control by authorities or predict.

All this is occurring at a time of extremely high global asset prices and still low economic growth relative to the past. Could we be vulnerable to a major asset price correction that creates the conditions for a crisis?

Global central banks have facilitated these elevated asset prices. A long series of global financial problems have now been passed through all parts of the financial system with most of these problems stacked up and now resting with central banks and Governments. The buildup of debt that this has created has forced central banks to keep yields at ultra-low levels, thus raising the prices of a variety of other global assets.

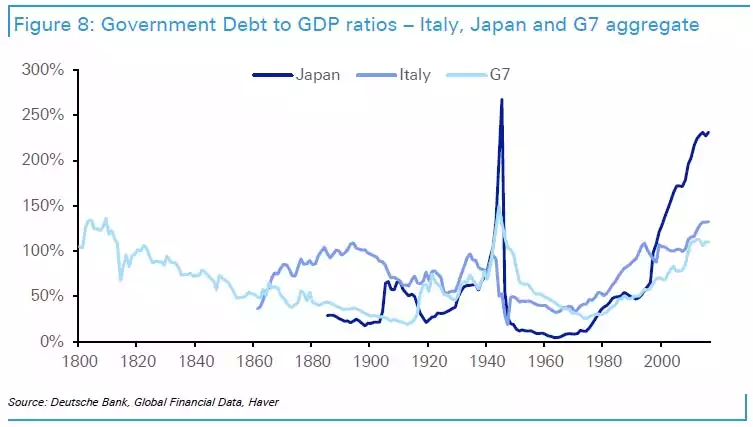

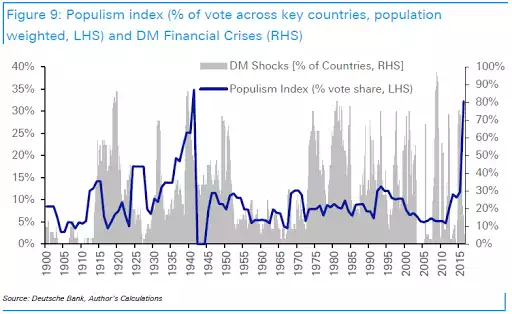

Italy and Japan have seemingly unsustainable debt burdens and are likely vulnerable to a crisis outcome. However both have had this for some time which mitigates short-term risks. Italy is perhaps more vulnerable because of precarious and fragile politics, elevated levels of populism and a central bank that is regional and not domestically controlled. Japan shows how long a crisis can be avoided but that doesn’t automatically mean we should be complacent, especially as the BoJ now owns over 40% of the JGB market (from under 10% in 2012).

On populism, our index (Figure 9) tracking its rise across key DM countries shows that we are close to the 1930s highs. Is this a precursor to a big crisis? Does it make for more unpredictable politics, economics and markets?

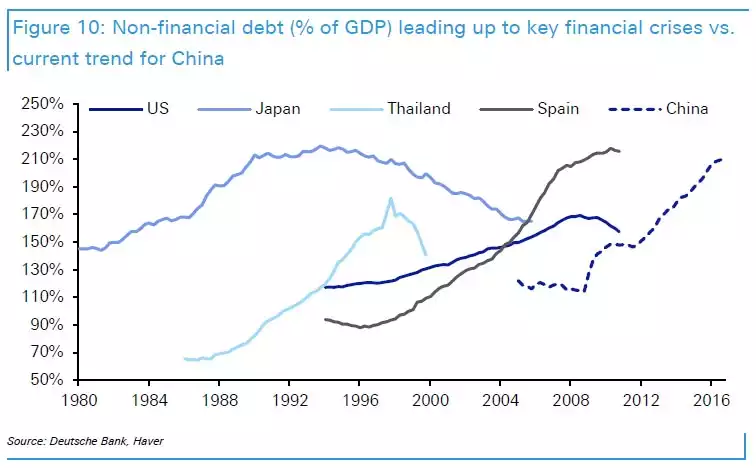

We see China’s credit growth post GFC as also an area of great concern. As an example, in a recent IMF report they analysed 43 global cases of credit booms in which the credit to GDP ratio increased by more than 30 percentage points over a 5-year period. Only 5 cases ended without a major growth slowdown or financial crisis immediately afterwards.

The IMF also caveated that these 5 cases, considering country specific factors, provided little comfort. If that wasn’t enough, the fund also points out that all credit booms that began when the ratios were above 100% ended badly.

These are perhaps the main observable risks out there but we go through a list of other potential catalysts in the piece. As we discuss at the top, by their very nature, financial crises or shocks are generally unpredictable.

While we can’t be confident of where and when the next crisis will occur we can be pretty confident that the conditions remain in place for a world of frequent crises.”