World’s Top 3 Gold Producers Fall in Q1 & Australia Closes the Gap on China

News

|

Posted 03/06/2021

|

7118

Amid a strongly rising gold price and renewed investment demand it is instructive to look at what’s happening with supply. After all, on the equation of supply, demand and price, increasing gold demand, as appears set to continue, may matter less if supply too is increasing.

We must at this point caveat that last statement with the reminder that new gold supply historically only increases by less than 2% per year. Whilst that establishes gold’s intrinsic value through rarity, the reality is that increased demand must be met through weaker hands giving up their share of the existing 180,000 tonne holdings. That high stock-to-flow ratio is fundamental to gold’s historic maintenance of value as we explained in January here. By comparison of course we saw the US create more US currency last year than in any year beforehand by increasing the total by around 25% in a single year. For all the statistics from COVID, surely that must be top 3 yet is rarely understood by most people. Yet.

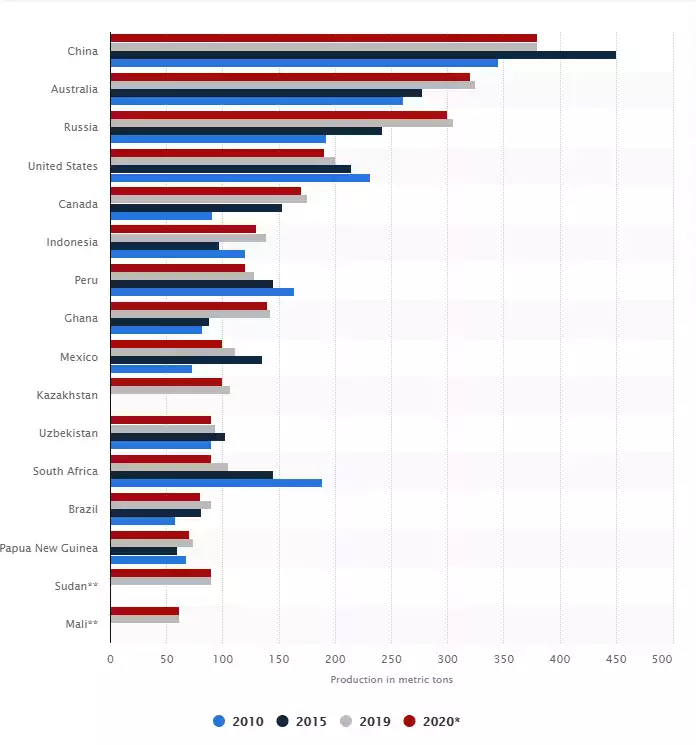

Last year saw Russia reportedly overtake Australia as the world’s 2nd biggest gold producer with 331 tonne just ahead of Australia’s 327 tonne and both closing the gap on the world’s biggest producer, China at 380 tonne. The chart below from Statista shows this (albeit with numbers not finalised for last year).

There is a reasonable amount of inconsistency when it comes to gold statistics, particularly out of opaque countries such as China and Russia so it all needs a pinch of salt. The latest statistics on gold from the independent (and so arguably more reliable) Australian consultancy Surbiton Associates for Q1 of 2021 show a continuation of falling supply but also on Australia and Russia continuing to close the gap on China. Surbiton appear unsure as to who is currently in 2nd place given the inconsistent numbers out of Russia. What is clear is that both Chinese and Australian production numbers have fallen sharply this last quarter, despite COVID disruptions largely past, and hence adding weight to the view that we have reached ‘peak gold’.

Chinese production dropped to 74.44 tonne (less than 300t annualised) according to the China Gold Association, 9% down on the same period last year which was largely arguably before the effects of COVID and China continues to struggle with tightening environmental regulations which have been slowing their production for a few years now.

Australia was very close to China at 74 tonne for the first quarter but down 9 tonne or 11% on Q4 of 2020 and worth $5.5b. Against the same quarter last year (as the March quarter is seasonally usually lower) it is 3 tonne or 4% less. Russia is reportedly also 4% down.

Below are the largest producers in Australia for the last quarter:

Cadia East 179,546 Newcrest Mining Ltd

Boddington 152,000 Newmont Inc.

Tanami 117,000 Newmont Inc.

Super Pit 111,278 Northern Star Resources Ltd

Fosterville 108,679 Kirkland Lake Gold Inc.