Will the RBA Need to Start QE?

News

|

Posted 02/07/2021

|

5446

The RBA meets this coming Tuesday to decide on interest rates and their program of Yield Curve Control. For an institution that has categorically said they don’t see rates rising until 2024, no one is expecting any change in rates next week. They are also already basically at zero (0.1%) and have also categorically said they won’t drop rates any further. That of course leaves the money printers… At a time when Jo Public seems to think everything is awesome, what do we expect from the RBA from here?

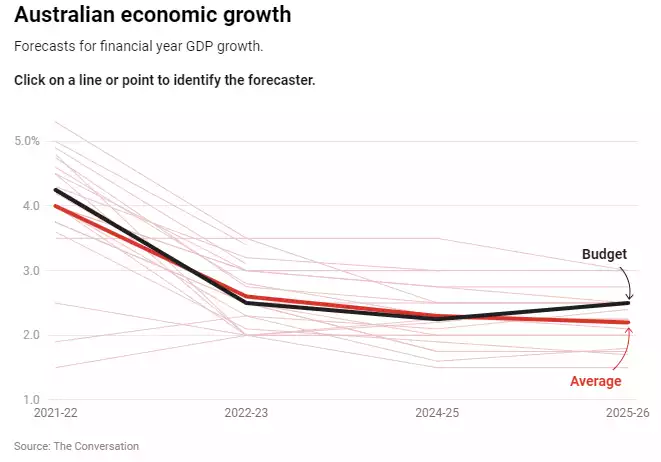

Yesterday we saw the annual report released for The Conversations July 1, a forecasting survey of 23 of Australia’s leading economists. From ABC News:

“On balance, the panel expects year-average economic growth (the measure reported in the budget) to slide from 4 per cent this financial year to just 2.2 per cent by 2024-25, well below the average of 2.6 per cent assumed in this week's intergenerational report.

The panel forecasts much weaker business investment than does the budget and lower household spending, but higher wage growth and lower unemployment. It expects a flat share market, and slower growth in house prices.”

Welcome to the RBA’s dilemma. Just as the headline act of the US Fed is stuck between rising inflation but clear signs of a weakening economy this half year and EVERYTHING inflated by cheap money, so it seams our RBA may be too. Charts like the following don’t scream its time to tighten and indeed will be screaming to the RBA that maybe they need to do more? The considerable spread of forecasts (each of the pale pink lines is one of the 23) also highlights how uncertain these times are, irrespective of peoples views around any comparisons between economists and weathermen… Critical assumptions around vaccination rates, borders reopening and immigration restarting have massive impacts and the 2 most bullish below basically assumed all of those are imminent…

The other concern for the RBA is the panel collectively saw these crazy high iron ore prices to stay for longer than the budget predicts which of course is bullish for the AUD… not something the RBA wants to hear.

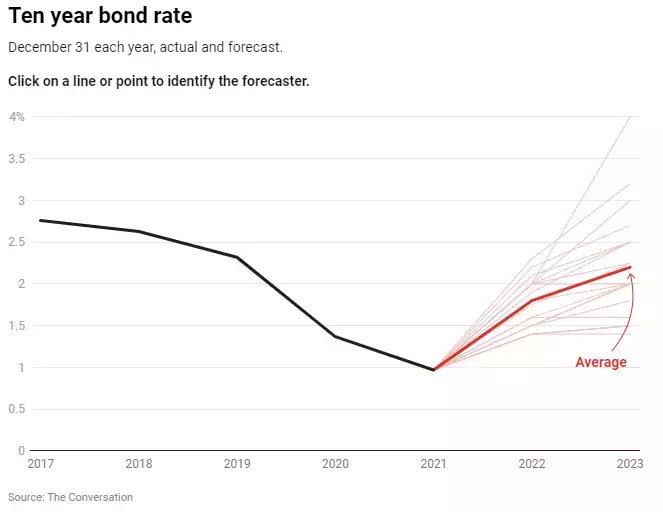

For an economy with one of the most bubble like housing markets in the world (challenged only by New Zealand, Canada and Switzerland) driven purely by low interest rates and rampant speculation, all eyes are on where interest rates are headed. There are 2 factors at play here. What the RBA wants rates to be and what the bond market decides they will be. Again from ABC News:

“Over the past year, the bond rate at which the Commonwealth government can borrow for ten years has jumped from 0.9 per cent to 1.5 per cent in accordance with moves overseas.

The panel expects further increases to a still-low 1.8 per cent by the end of this year and to 2.2 per cent by the end of next year.

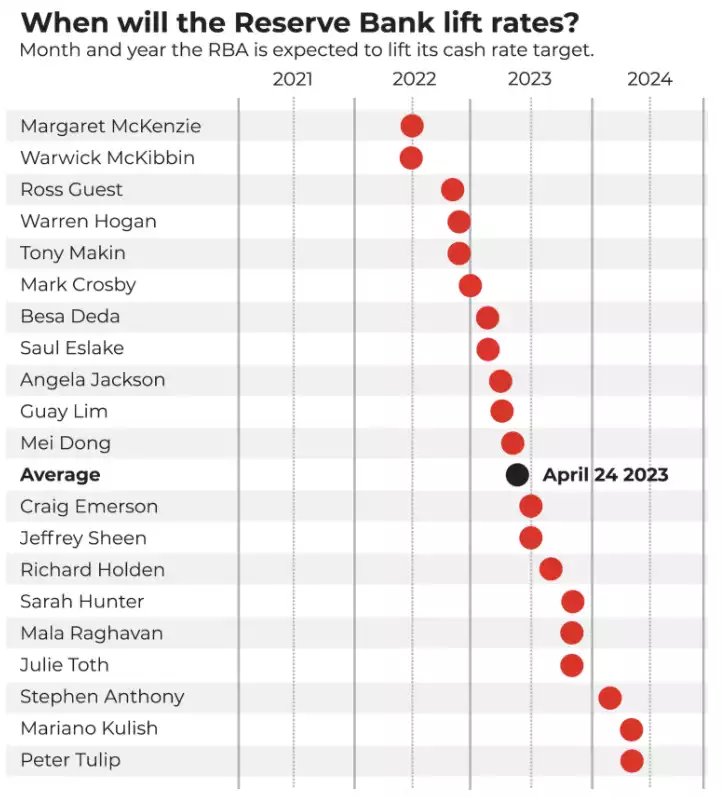

Even so, the panel expects no increase in the Reserve Bank's cash rate — the one that drives variable mortgage rates — for almost two years, until April 2023.”

So how about government’s “bold prediction” of 12.5% non mining business investment beyond this year? The panel saw that being less than half at just 5.8% but importantly gave the reason of not just low population growth but also because the government has already sucked forward all it can. You could apply this same logic to the Aussie property market that has sucked forward a pile of demand through grants, incentives and of course record low interest rates. With little foreseeable population growth how does such a Ponzi scheme survive? Sydney just saw 3.8% property price growth in the single month of June, nearly double wage growth for an entire year. How is that sustainable?

Speaking of sustainability, how about government deficits?

“This year's budget forecast is for a deficit of 5 per cent of GDP after last year's near-record 7.8 per cent of GDP.

Asked at what point over the next four decades the budget deficit would shrink to 1 per cent of GDP, three panelists replied "never".

Six others said not before 2030. Only four nominated the decade ahead.”

Sustainable?

Rising inflation and a slowing economy leads to stagflation and that will not be tolerated.

The RBA is facing a worsening picture. It has nowhere to go on rates, its yield curve control program has its limitations if borrowing slows, and that leaves outright QE to keep things suitably ‘accommodative’. But will the introduction of QE amid the Jo Public perceived goldilocks economy spook the market?

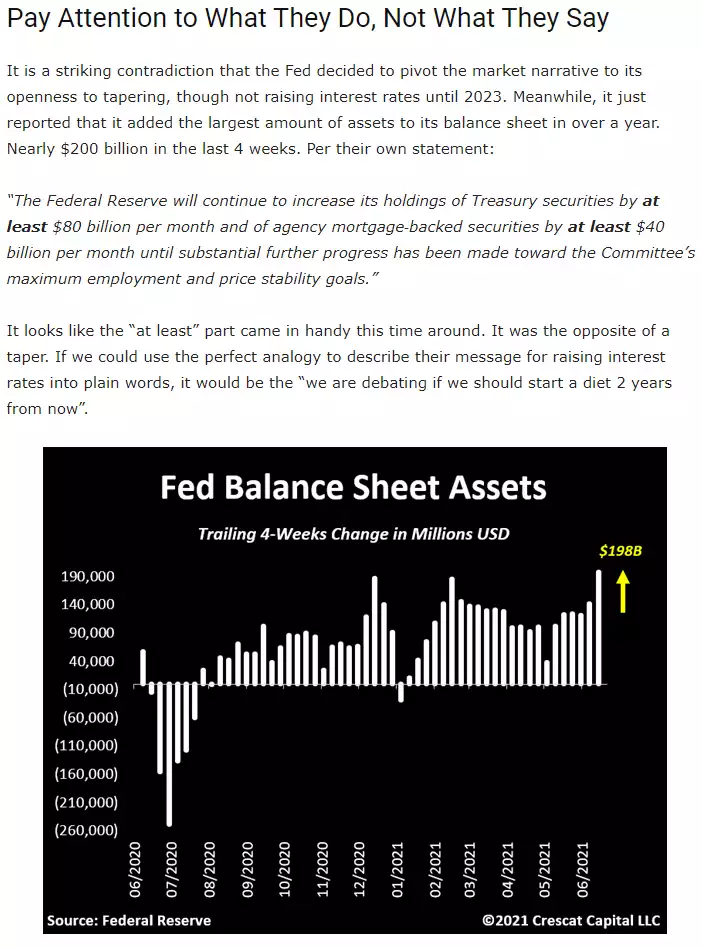

You can of course follow the Fed’s lead and say one thing and do the other…. The following is an excerpt from a recent Crescat article and a fitting way to leave you: