Why IMF says we’re “teetering on the edge”

News

|

Posted 27/07/2022

|

7400

Right on cue for the so called, and much anticipated, “Fed Week” where the market is on tenterhooks on just how much the US Fed will raise rates tonight, the IMF lobbed in a hand grenade last night stating the world economy is “in a very critical moment here”. Today of course also sees our own inflation figures released with economists predicting a 32 year high 6.3% print, getting ever closer to the RBA’s prediction of 7% before year’s end.

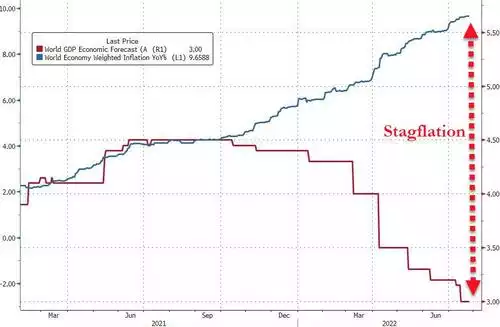

The IMF slashed its global economic growth forecast for the third quarter in a row whilst simultaneously raising its inflation projections in unison spelling out an ugly stagflationary picture at this critical juncture for central banks. On Monday we discussed the very clear recession signs for both the US and Eurozone. The chart below shows the enormity of the disconnect the broader world is currently staring down the barrel of, prompting the IMF to state the economic outlook is “overwhelmingly tilted to the downside” and "may soon be teetering on the edge".

And so Jerome Powell and his ‘merry men’ of the Fed FOMC are staring down the barrel of tightening into a recession and in so doing both guarantee the outcome and exacerbate the effect. IMF’s chief economist empathised in an interview afterward:

“We are in a very critical moment here…..It’s easy to cool off the economy when the economy is running hot. It’s much harder to reduce inflation when the economy is close to a recession.”

That the market is torn on whether the Fed will hike by 100bps or 75bps tonight, the plethora of bad data and reports like this must surely be weighing heavily on them. So too, however, the weight of the effects inflation is having on the US economy. US economic commentator Michael Snyder yesterday spelt this out in simple real terms with “14 Signs That The US Economy Is Poised To Crash Really Hard During H2 2022…

#1 One survey that was just released discovered that 35 percent of all small business owners in the U.S. “could not pay their rent in full or on time in June”.

#2 A different survey found that 51 percent of all small businesses owners in the U.S. believe that rising prices could “force them to close their businesses within the next six months”.

#3 It is being reported that 45 percent of all small businesses in the U.S. have already decided to freeze the hiring of new workers.

#4 Sales of previously owned homes dropped 5.4 percent during the month of June. That is now the fifth month in a row that we have seen a decline.

#5 In three-fourths of the metro areas that Redfin tracks, at least 25 percent of home sellers reduced their asking price during the month of June.

#6 Blackstone has prepared a war chest of 50 billion dollars so that it can scoop up depressed real estate all over the country after housing prices have crashed in the months ahead.

#7 The number of Americans applying for jobless benefits has risen to the highest level in eight months.

#8 Employment postings for software development jobs have dropped off by more than 12 percent during the past four weeks.

#9 The Conference Board’s index of leading economic indicators has now fallen for four months in a row.

#10 The S&P Global Flash U.S. PMI Composite Output Index just went negative for the very first time since the last recession.

#11 The latest number for the Philadelphia Fed manufacturing index came in at -12.3, and that was much worse than what most experts were anticipating. Any reading below zero indicates contraction, and needless to say this reading was way below zero.

#12 Inflation continues to rage out of control even as economic activity in the U.S. significantly slows down. If you can believe it, the average price of a used vehicle in the United States has now risen to a whopping $33,341.

#13 The Atlanta Fed is now projecting that U.S. economic growth for the second quarter will come in at -1.6 percent. If it is ultimately confirmed that the U.S. economy has already been contracting for two quarters in a row, that would mean that we are officially in a recession right now.

#14 Thanks in part to the rapidly tanking economy, Joe Biden’s approval rating has plunged all the way down to 31 percent.”

As we discussed last week, our own RBA has a similar dilemma. A 6.3% print would be more than double the 2.4% wage growth figure putting real pressure on ordinary Aussies. At the same time these same ordinary Aussies have massive mortgages and will struggle to service that debt with the same higher rates ‘required’ to stem inflation. We say ‘required’ as it is highly questionable whether rates can blunt inflation caused largely by supply side constraints and the self, inflation-fulfilling human behaviour of ‘buying now before the price goes up’… sending prices up… Oh, and its not just our personal debt that is the problem. From our new Treasurer himself:

“A trillion dollars in debt costing more and more to service means that we have to be upfront with people. We can’t do everything that we would like to do. We can’t even afford the good ideas that people put to us. And so we have to prioritise.”

Cue Mr Albanese: “This year will be tough.”

What seems to be becoming abundantly clear is that stagflation is not going away any time soon. Yes a recession will reduce demand somewhat, but will it truly kill inflation that will not have been fully addressed before central banks are forced to pause or pivot on their monetary tightening agenda?

Wall Street was all red again last night but at some stage soon, the forward looking markets are going to price in this inevitable turn of policy and the deeper negative real interest rates to come. We may then again see the previous loose-monetary-policy-amid-weakness dynamic that saw gold, silver, crypto and tech shares soar.