Raising rates with or without the Fed

News

|

Posted 16/09/2015

|

4009

Recently we have been providing some perspectives from metal and market analysts on this week’s FOMC announcement. It is certainly a topic that has dominated the news in recent days and for every article or opinion piece that suggests that rates will finally lift this week, there seems to be another claiming the opposite. Kitco news has sensibly capitulated, calling it “a toss-up”. GATA director Ed Steer said overnight that “guessing whether the Fed hikes rates on Thursday is something of a futile exercise because even the rate setters appear to be wavering and the decision will probably come down to the wire”. For something a little different then, today we look at an interesting development from the Pendleton Community Bank (PCB) in West Virginia; a 90 year old institution with 5 branches which is currently seeing “increasing loan demand” and is concerned about it.

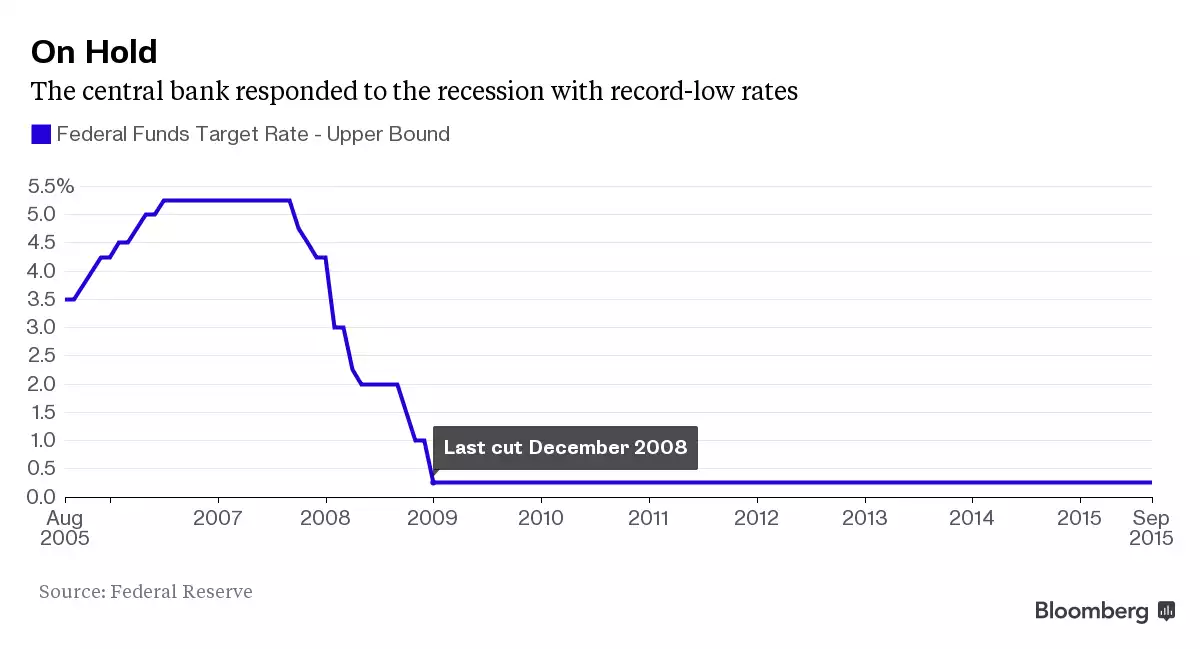

The bank’s CEO, Bill Loving, has identified a need to start raising deposit rates to account for this demand irrespective of the Federal Funds Rate decision. The demand is being seen for both residential and business applications and is a consequence of accommodative ZIRP (Zero Interest Rate Policy) which was introduced in December 2008 as the graph below illustrates. The PCB states that a continuation of this policy will squeeze their lending margins. What’s interesting is that as community banks rely heavily on deposits in order to provide loans, the supply and demand of loanable funds has the potential to spark competitive behaviour between the PCB and its peers on both the deposit and loan side of the business. In fact, the PCB’s website openly claims “we want to be your bank”, going as far as utilising the web address yourbank.com rather than one that reflects the bank’s name.

With current PCB savings rates at 0.05%, there is an established trend of depositors shifting to higher risk investments in a hunt for yield and this behaviour can be viewed as a risk to the business model of such small lenders. With low rates being so destructive for savers, the bank’s CEO was quoted as saying “I think it’s time for the Fed to move” and in the absence of such a move, free market forces may very well implement this outcome in isolation.

In a way, we can see parallels back home in terms of APRA’s move to curb investment property lending and the subsequently publicised increases to investment property and interest only loan rates. Although the motivations differ in this example, one could make a case that these rate increases are a consequence of a pattern of concentrated investment demand in a protracted low-yield environment that has required a rate response. The endless speculation over FOMC decisions may be hence becoming less relevant if we start to see a rate divergence in response to financial realities.