Junk Bonds – Early Warning Sign

News

|

Posted 18/02/2016

|

5284

The zero rate environment engineered by central banks since the GFC was meant to entice old and newly printed money into risk investments to spur along growth. One sector in particular that benefitted from this reckless hunt for yield was high yielding bonds/debt, otherwise known as junk bonds, to the tune of $1.8 trillion! Because these loans had secondary security they yielded well to reflect that risk. It was all going swimmingly until oil tanked and global growth slowed and we started seeing more credit rating downgrades and even outright defaults.

So not surprisingly the investors are realising the debt they are holding is becoming worthless and want out. And oh are they getting out… As we’ve explained with sovereign bonds (US Treasuries etc) there is always the inverse relationship of bond price and yield. So when people rush for the door, the price goes down and the yield goes up (effectively to entice new buyers and keep the ‘hopefuls’).

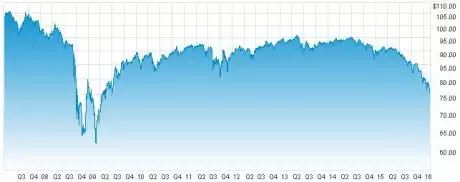

To help mum and dad investors into this space (subprime MBS’s anyone?) there are even ETF’s that provide a vehicle in. The graph below shows clearly the recent outflows from HYG (just one of them but indicative of others). You may notice the last time it did this was the GFC.

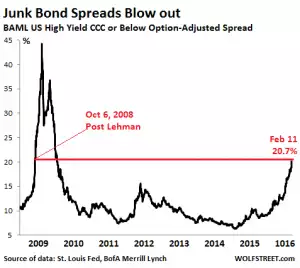

More tellingly, the following graph shows the yield spread which likewise is in an exponential rise, ala GFC. (this is a worthy addition to our recent collection of parabolic charts here, here and here).

Whilst these charts alone are instructive from a history repeating perspective, the mechanics of why are actually simple. The debtor corporations who have resorted to these loans (of which the buyers of the bonds are the creditors) quickly become unable to manage the exponential rise in the cost of that debt, especially as their earnings suffer in this near recessionary environment. When you consider nearly 20% of it is energy related and oil is at historic lows and often below the cost of production, you quickly see the problem. It also in part explains why they keep pumping and selling oil at these prices (and exacerbating the supply problem) as they need more cash to service this ever increasingly expensive debt. It’s a death spiral. Defaults inevitably jump and those yield spreads follow suit until we see again what happened in the GFC. This time however it is likely to be much much worse.

It explains why many analysts see sky rocketing junk bond yields as the early warning sign of a looming financial crash. They are the canary in the coal mine oil well.