How the Fed will tear apart the economy

News

|

Posted 03/02/2022

|

7258

Today we explore a bit deeper into the view held by many respected analysts that the US Fed, and certainly by extension our own RBA, will be tightening policy into an economy or business cycle coming off its peak… i.e. the very worst time to be doing so.

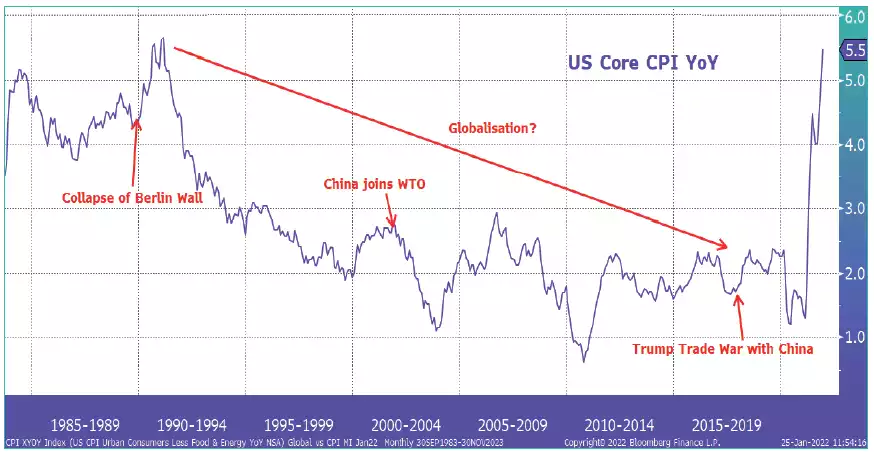

One of the smarter minds we respect is Macro Insider’s Julian Brigden. For some time Brigden has been talking about the very macro phenomenon he calls the Great Moderation. In essence, starting with the collapse of the Berlin Wall then China’s entry into the WTO and resulting globalisation, the world went thought a quarter of a century of “a halcyon period of unbridled capitalism, disinflation and critically, lower economic volatility.”

That of course has changed, had started to change evidenced by Trump and Brexit, but now with COVID was a big catalysing agent.

“Driven by inequality, social unrest and underpinned by shifting demographics, voters in the West were beginning to demand change. Furthermore, even our political and corporate masters were beginning to question the logic of handing the keys to the kingdom to China.

Hence our contention that these slow-moving dynamics (such as aging demographics, which support higher bond yields) would have ended the Great Moderation on their own. In that sense, Covid was simply a powerful accelerant.”

Brigden talks to research done around the causes of economic shocks and inflation. In short, history is littered with exogenous forces entering a market at exactly the wrong time and become ‘procyclical’ so as to exacerbate or amplify the sorts of cycles depicted above. He provides the metaphor of the famous Tacoma Bridge where, simplistically, the frequency of the effects of the wind matched the natural frequency of the bridge and ‘harmonic’ or ‘mechanical’ resonance occurs. If you’ve never seen the footage of the outcome you need to watch it, particularly with the current economic metaphor firmly in your mind:

https://www.youtube.com/watch?v=XggxeuFDaDU

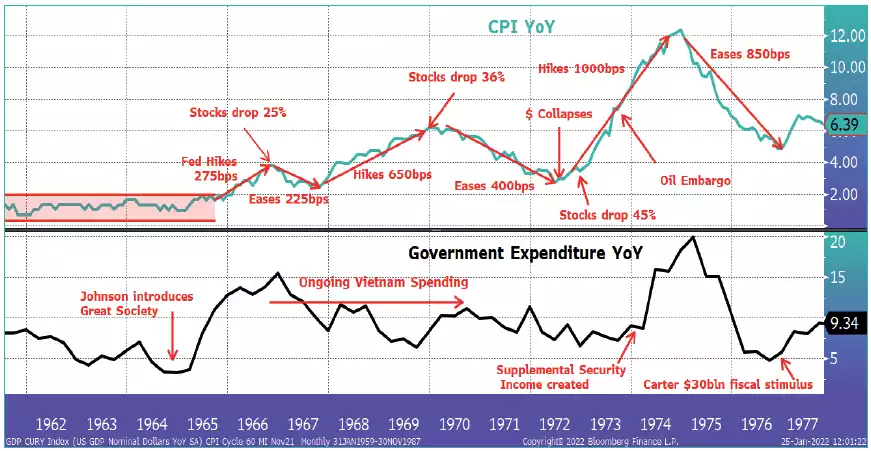

Brigden provides the very familiar historical example of the second half of the 60’s “when concurrent policy errors coalesced to end the longest period of stable inflation in the post-war period.”

“The first “error” was Johnson’s Great Society spending in 1965, which hit an economy already operating close to capacity as the Vietnam War ramped up.

The second was a Fed, that initially thought they could run ‘a high-pressure economy’ with higher wages in order to draw workers back into the market.

Sound familiar? But as inflation accelerated, they changed their mind abruptly and tightened policy. Unfortunately, their tardy response hit an economy that was already peaking. The subsequent equity and housing drop just added to the volatility - resonance. What followed was more of the same, with policy increasingly reactive and buffeted between successively higher inflation and increasingly dynamic market gyrations. Far from dampening cycles, poorly timed, reactive policy added to cyclical amplitudes.”

The results below are plain to see… In December 2021 ex Fed President Kocherlakota raised the risks of rising inflation and the need for an immediate aggressive Fed response warning… you guessed it, ‘The Fed Faces a Troubling 1965 Parallel’….

But of course the Fed procrastinated and simply talked about tapering.. not rate rises, not QT, just less of more new money. That means the response will need to be both more aggressive and ill timed.

Ex NY Fed President Dudley recently warned:

“So how high will rates need to go? This depends on how easily higher rates will tighten financial conditions and cool off the economy. So far, there’s little sign they’ll have much effect. All this suggests, the Fed will have to raise short-term rates by considerably more than what’s currently anticipated.”

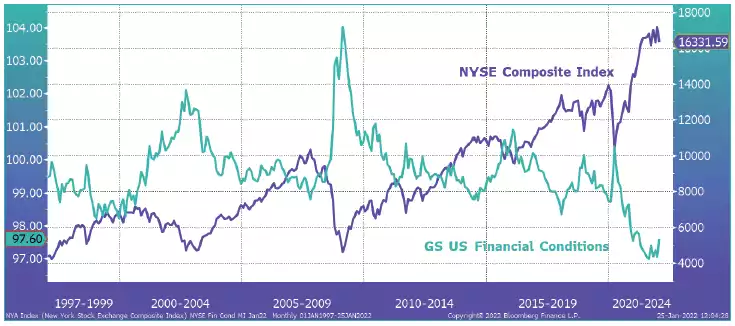

The chart below illustrates clearly just how completely distorted the current set up is with the blue line US shares as a proxy for the economy and green line how loose or tight Fed policy is. Never looser, never more over heated.

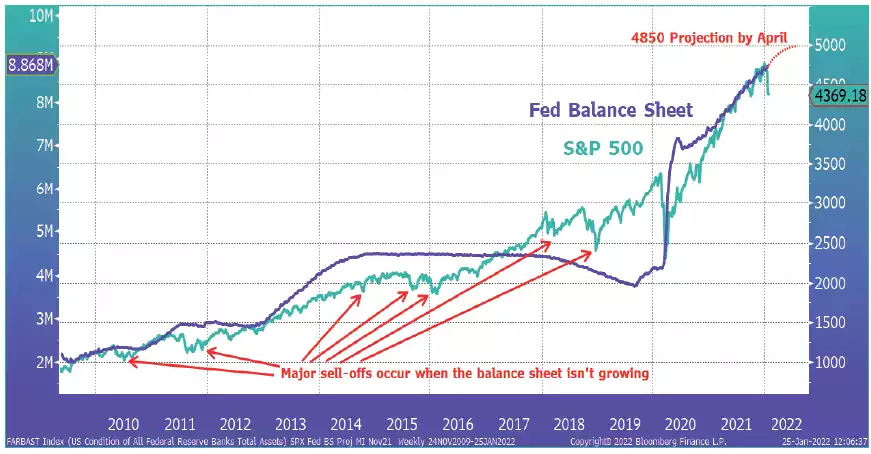

Now lets remind ourselves of the relationship between US shares and money printing via QE.. Ala print money = shares go up, stop = shares go down, tighten = major corrections…

Brigden then cites a recent research paper that “$100bn of “new money” would increase the stock market value by $300-$800bn” and “that the value changes are permanent so long as a flow is not removed, if the balance sheet declined, aka QT, the multiplier effect to the downside would be just as great.” Digest that for a bit..

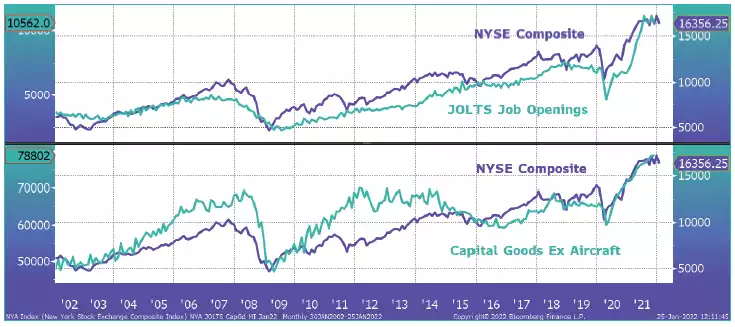

The real kicker is that the “hyper-financialisation of the real economy means that any correction in stocks will quickly manifest itself both in soft indicators such as confidence and in concrete metrics like employment and CapEx.”

These charts are critically important. There is now a clear correlation between the sharemarket and unemployment as well as manufacturing and capex.

We have just seen the worst start to a year for US shares since 2009 during the GFC. May we remind you that was on the announcement they would likely soon raise rates by a measly 1% (4 x 25bp rises this year)..likely… and maybe reduce the Fed balance sheet via QT… maybe.

Brigden’s sparring partner, Raoul Pal is firmly of the view that we are about to see a dramatically slowing economy coinciding with this. Again, resonance.

And so here we are with markets rebounding over the last 2 nights on hopes none of the above is real and that we ‘only’ see 1% in total and spread out with the latest Fed commentary hinting at a ‘calibrated approach’ to raising interest rates to fight high inflation. i.e. the market may be realising that more than 1% was priced in, history shows they will reverse if the markets tanks anyway, and hence ‘buying the dip’. And so, again, we are in for a volatile ride ahead as this cognitive dissonance dance continues. Don’t get sucked into these ‘everything’s awesome’ rallies…. Refer previous metaphorical bridge…

Tomorrow we share part 2 of this excellent piece of work from Brigden where we bring in that elephant into the inflation room, inventory, and how it historically fits in these economic and business cycles.