Goldilocks & the 3 Debt Solutions

News

|

Posted 10/08/2022

|

7819

The world is sitting on an unprecedented amount of debt. There are only 3 ways to reduce debt. You can to pay it off through increased ‘profits’ or productivity at a sovereign level, write it off (pretty much impossible at a sovereign level – particularly if you are the worlds reserve currency and need ‘faith’ preserved in said currency), or finally via inflation. In simple terms if you let inflation rip then relatively, your fixed amount of debt looks lower against everything else now ‘worth’ more. So the question begging now is – wouldn’t the Fed quietly like some Goldilocks ‘not too hot, not too cold’ inflation?

Respectfully, blind Freddy can see the US is in a recession whether you believe 2 consecutive quarters of negative growth defines one or not. The US NFP jobs report Friday, heralded by recession sceptics / spin doctors as proof of no recession, when looking under the hood, perversely confirms the recession is here as we discussed yesterday (article and discussed on GSS Insights). So lets take a miraculous turn of growth to pay down all this debt firmly off the table. Lets also remove an equally miraculous universally agreed debt jubilee off as well. The world, quite frankly, is too divided to agree on something that will disproportionately see winners and losers of an historically epic monetary scale. So we are stuck with inflation or an inevitable financial bust and economic reset that has ended every Fiat currency experiment in history.

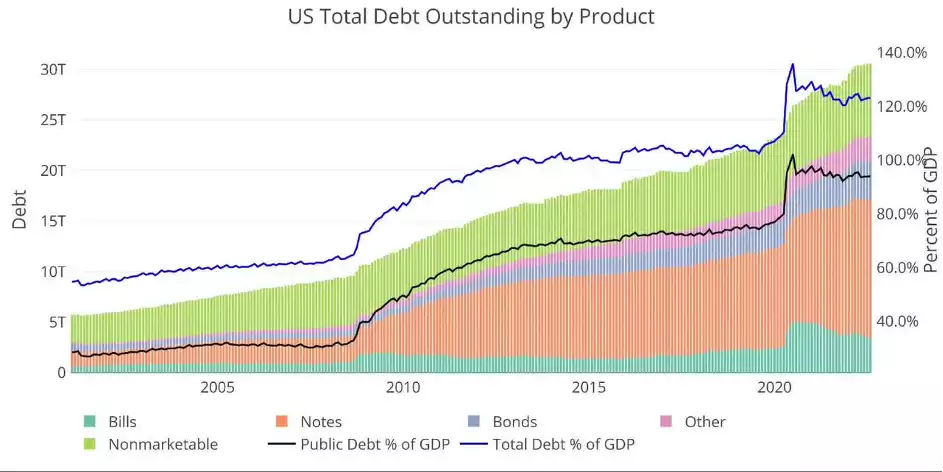

What is often missed in this fanciful theory of inflating away debt is our lack of political appetite for any kind of austerity or hardship. This week we saw the US Government pass yet another piece of big spending legislation via the Climate and Drugs Bills, another $437 billion in total on top of all the previous debt funded programs to ‘help’ the economy and, lets face it, remain elected. Despite the supposed responsible slow down in spending by the Biden administration, the US Treasury has added more than $1 trillion in debt in the first 7 months of this year! The US public debt is now $30.6 trillion and so the 23 bps weighted average increase in interest rates on that debt already this hiking cycle equates to an EXTRA $70 billion. Note in the graph below too that US debt still sits at over 120% and with the addition of more debt and the reduction of the GDP denominator, that looks set to rise yet again.

And so if you are still spending more than inflation you are doing absolutely nothing to reduce your debt in real terms. Many social benefits paid out are linked to CPI but the Fed chooses the always lower PCE deflator as it’s measure of achieving its ‘2% target’. Cynically that lower measure allows real CPI to run hotter for longer to try and fight that debt metric as well. You can see the conundrum here. Whilst the Fed might like some stickier real inflation to combat the debt levels, it is trapped into raising rates whilst headline inflation is hurting so many. That very rate rising tool is causing recessionary pressures, more interest payment burden and is still woefully less than inflation. Negative real interest rates, where the nominal interest rate less inflation is negative, essentially ‘forces’ people not to save (as you are literally going backwards in cash in the bank) and to spend or invest in risk. That helps growth but you can clearly see it doesn’t help keep down inflation. That’s why negative real interest rate environments are usually constructive for gold and silver. Whilst they don’t yield, they are the perfect hedge against the resulting inflation and financial instability that protracted periods of negative real interest rates inevitably end in.

There literally is NO Goldilocks solution to this mess.

The author of the graph above, SchiffGold, summarise nicely:

“What it means for Gold and Silver

While the market continues to see the current Fed as being “tough on inflation”, Powell is a far cry from Volcker, with real interest rates still very negative. Even though negative real rates will do little to combat raging inflation, they will do plenty to upend anyone sitting with a lot of short-term or adjustable-rate debt. Look no further than the US Treasury for the biggest party at risk.

A strong July jobs report has given the Fed more room to deny recession and take another aggressive rate hike in September. The Fed is moving very quickly and the math is just starting to catch up. The Treasury could quickly find itself paying more than $500B in annual interest payments. What then? What if inflation is still high? Can the Fed keep hiking and send the US government into a debt spiral while also destroying the value of their own balance sheet?

This seems unlikely at best. The Fed has to pivot because it mathematically has to! This is the same reason interest rates are not above the rate of inflation today. They can’t be! The US Treasury, along with every other over-stretched borrower, would go belly up. The Fed won’t let this happen.”

GOT A QUESTION about today's news?

This afternoon, the Gold & Silver Standard Insights team will be breaking down the news and answering YOUR questions.

Submit your question to [email protected] and SUBSCRIBE to the YouTube Channel to be notified when the GSS Insights video is live.