Gold Lifts Russian Reserves

News

|

Posted 05/04/2016

|

5133

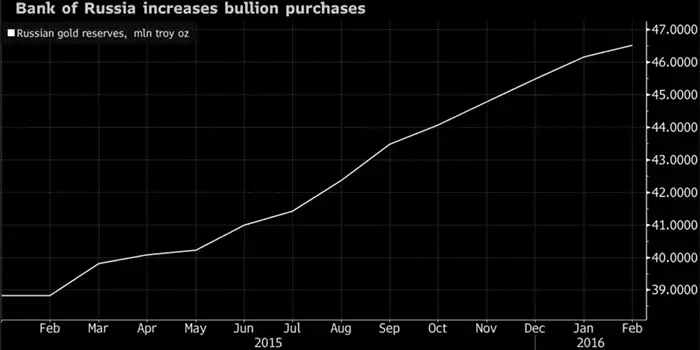

We have been frequent reporters on Russia’s national acquisition of physical gold; something that was engaged in with particular vehemence in the latter part of last year. In 2014, Russia was forced to draw down on its reserves, utilising around 20% in support of the Ruble at that time. We noted late last year that such actions are often due to a multitude of factors including sanctions, currency devaluation and falling oil prices and we reiterate that Russia’s gold acquisition is contrary to what we typically expect to see in the case of foreign reserve drawdowns – which is a tendency to halt acquisition or even liquidate gold reserves.

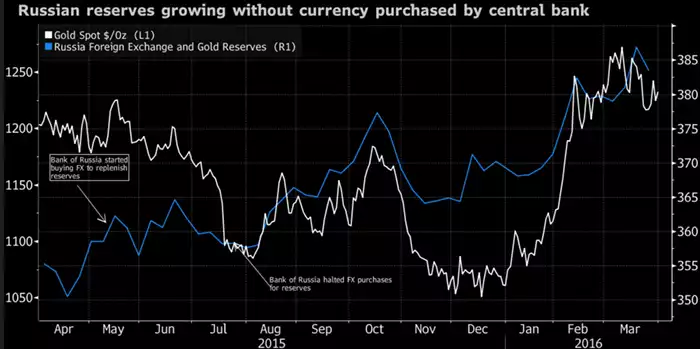

This year on the other hand has seen an approximate 9 percent rally in the Russian currency which has given support to the idea that the country would again start foreign currency purchases after a hiatus of approximately three quarters.

It appears that Central Bank of Russia head Elvira Nabiullina is in no rush to do so however. Gold’s recent stellar performance which we reported on last week has bolstered Russia’s reserves to a level now exceeding $380 billion. This gives the nation some flexibility to delay foreign currency purchases in their pursuit of a $500 billion reserve target. According to a recent survey of economists, Nabiullina is likely to wait for something in the vicinity of a 12% increase in the Ruble which would mean a 60 to the dollar level (it is currently just under 69) prior to the resumption of foreign-exchange market involvement.

The period of time since efforts to restock reserves were halted has seen an incredible 7 percent increase in total Russian holdings; something that has been largely achieved simply by the appreciation of its gold purchases which themselves have increased 12 percent in that time. The following chart illustrates this scenario.

An important takeaway here is that the flexibility and diversity that physical gold has provided Russia is directly applicable at the individual level.