Gold’s Reaction to Fed’s Confusion

News

|

Posted 12/10/2015

|

4126

The last FOMC decision on rates 3 weeks ago was somewhat unique in that it was one of the most anticipated of all time. We commented on this during the lead up and highlighted former Chairman Greenspan’s comments of bewilderment at the time relating to how baffling it is that “a few basis points in an overnight rate by one central bank is going to be all determinate”. Subsequent to the release of the decision, we reported on how the response was comprised of an ongoing bolstering of gold acquisitions at a national level and an apparent decline in faith considering that the once somewhat consistent forward guidance has been replaced with mixed messages.

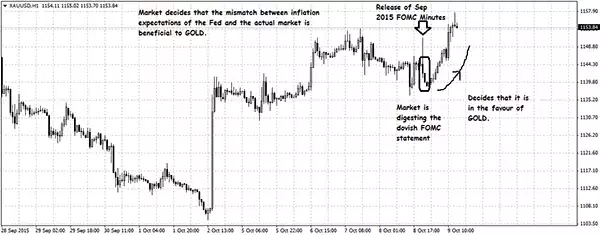

Last week has provided indications of this trend continuing on the back of the release of the FOMC minutes which we touched on in our weekly wrap of last Friday. The gold price rallied from the open in New York on Thursday evening to a close of US$1,156 having hit a high tick of US$1,159 in the December contract with reasonable volume. Today we bring you commentary from the trading community which has drawn a correlation between the confusing message presented by the minutes and the appreciation in gold last week.

The idea revolves around a discrepancy between the inflation projections perceived by the fed and the reality of inflation conditions. The XAU chart below is annotated with suggestions as to the cause of the gold price movement in relation to the timing of the release of the minutes. The initial period post-release shows a drop in prices which commentary suggests is a reaction to the conflicting hawkish and dovish content within the minutes. Lack of direction and consistent forward guidance tends to foster a “selling” mentality as an immediate reaction.

An example of the hawkish tone in the release was the observation that "growth in real GDP over the first half of the year was stronger than participants expected when they prepared their June forecasts, and the unemployment rate declined somewhat more than anticipated". On the other hand, there was concern evident regarding the unexpected lack of inflation and furthermore, the previously prominent concept of this inflation-poor environment being transitory has been seemingly abandoned. The release stated that "participants anticipated that recent global developments would likely put further downward pressure on inflation in the near term; compared with their previous forecasts, more now saw the risks to inflation as tilted to the downside."

To summarise, the FOMC sees a failure in attaining their inflation target mandate of 2% despite extending projections out to 2018 and despite apparently improving economic data upon which they claim to operate. As such, the bias of the FOMC minutes would appear more dovish than initially interpreted in terms of inflation concerns and online commentary suggests that “once that confusion cleared 3 hours later, gold soared”. Although market behaviour is seldom the consequence of a single factor, this suggestion does act to highlight one of gold’s many endearing qualities; namely that of an inflation hedge and certainly there is merit to this idea considering that mainstream commentary is now squarely focused on further easing initiatives.