The Peril of Passive ETF’s & Breadth

News

|

Posted 12/01/2022

|

7030

There appears a large portion of economic forecasters predicting that 2022, whilst more volatile than normal, could see continued strong gains in US shares despite the still sky-high valuations. Already this year we have seen some large losses on US shares and then a strong rally like last night. Last night everything went up except the USD and all on the back of Fed chair Powells virtue signaling of ‘we’ve got this’.

Equities buyers saw ‘the Fed has our back’, bonds, gold and crypto buyers saw no quick fix and more debasement of fiat (reinforced by the USD dropping) and the inevitable outcome of his saying they will look to reduce their massive $8.77 trillion balance sheet. His call of Quantitative Tightening came with the warning “The balance sheet is much bigger and so the runoff can be faster. So I would say sooner and faster -- that much is clear,”… We all know what happened last time they tried QT…

The same economic forecasters are largely calling a short sharp correction any time soon but many go on to say the Fed will simply step back up to the plate and the TINA trade will see money pile back in and a resumption of gains, much like 2020. When they tried QT in 2018 we saw a 20% correction.

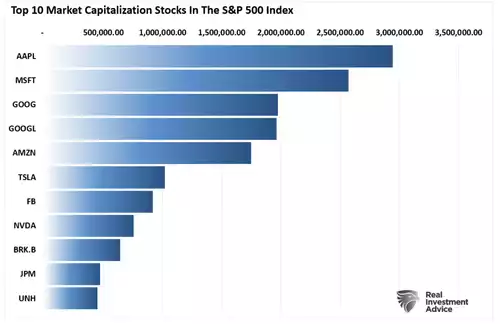

However Lance Roberts of RIA recently reminded us of the sheer scale of both that top 10 of the S&P500 and the predominance of passive index driven ETF’s blindly following.

“Notably, except for the Dow Jones Industrial Average, the major market indexes are weighted by market capitalization. Therefore, as a company’s stock price appreciates, it becomes a more significant index constituent. Such means that prices changes in the largest stocks have an outsized influence on the index.”

“Currently, the top-10 stocks in the S&P 500 index comprise more than 1/3rd of the entire index. In other words, a 1% gain in the top-10 stocks is the same as a 1% gain in the bottom 90%.”

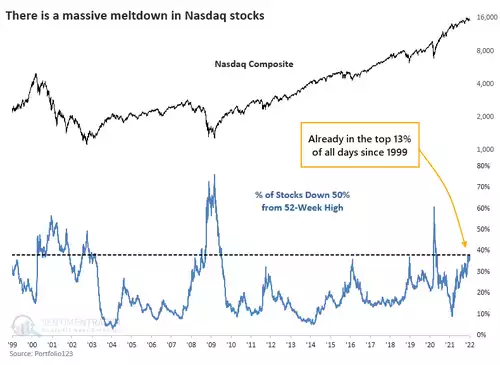

This top 10 is hiding a very big problem… From Sentiment Trader:

“After Wednesday’s post-FOMC selloff, more than 38% of stocks trading on the Nasdaq are now down 50% from their 52-week highs. Only 13% of days since 1999 have seen more stocks cut in half.

At no other point since at least 1999 have so many stocks been cut in half while the Nasdaq Composite index was so close to its peak. When at least 35% of stocks are down by half, the Composite has been down by an average of 47%.”

The last sentence is put into stark contrast against an index at near all time high….

This largely comes down to the fact that around a quarter of all ETF’s comprise that top 10. ETF’s are marketed on performance so they are ‘all in’ that top 10 to attract your money. We wrote about this lack of breadth recently here.

What most participants forget is that these ETF’s have to buy the actual shares and those actual shares need to be sold when the market index turns. This dumps a quite extraordinary amount of shares into a market all at once with few buyers. Liquidity becomes a massive issue. Roberts concludes:

“Despite the best intentions, individual investors are NOT passive even though they invest in “passive” vehicles. Eventually, some exogenous, unexpected event will change investors’ “speculative” psychology. When the psychology changes from “bullish” to “bearish,” the rush to liquidate entire baskets of stocks will accelerate the decline making sell-offs more violent than what we saw in the past.

This concentration of risk, lack of liquidity, and a market increasingly driven by “robot trading algorithms,” means reversals are no longer a slow and methodical process but rather a stampede with little regard to price, valuation, or fundamental measures as the exit becomes very narrow.

March 2020 was just a “sampling” of what will happen to the markets when the next bear market begins.”

In other words, whilst many commentators openly expect a market correction given the overbought nature of it, they then seemingly dismiss it as a ‘blip’ like we saw with the COVID crash in 2020. Roberts’ argument that that may not be the case this time appears to have a lot of merit.