Markets Have A Long Way to Fall

News

|

Posted 23/03/2020

|

24342

Yesterday saw our PM announce an unprecedented financial rescue package to try to soften the damage of business closures and unemployment. It is often inaccurately being called stimulus. This is in no way stimulus, this is damage control. But what it will be doing, as stimulus does, is inject a whole lot of new ‘free’ money into the economy that at some stage will find its way to inflation. To be clear though we will be in deflationary times first.

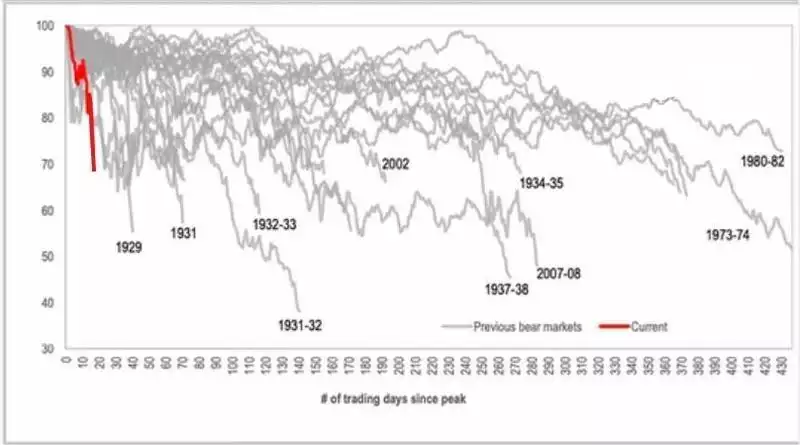

Last week saw the Fed unleash the biggest weekly injection of stimulus ever, nearly 2 times bigger than any week during the GFC. So how did that go? The biggest weekly fall on the Dow Jones since the GFC and if looking at the last month, the biggest since the Great Depression. The following is an excellent summary of where we are now compared to 100 years of the Dow Jones, the pace is unprecedented…

COVID-19 is the very definition of a Black Swan event, one that no one could have foreseen. But what such events do is draw out the tide and expose who’s been swimming naked. They also strip away the stimulus based pricing to see things return to fundamentals. The following charts illustrate this clearly.

Firstly let’s look at the Fed’s balance sheet (i.e. how many bonds they bought using freshly printed USD under the guise of QE) since the GFC. You will note the remarkable correlation until the disconnect in 2016. It shows that their notQE Repo market operations have taken the balance sheet back to $4.3 trillion already. That worked for a while, but….

That same 2016 onwards surge happened in an environment of weak corporate earnings seeing P/E multiples explode. As has happened before, that eventually corrects to what share pricing should be – an investment in earnings of a company.

More broadly than corporate earnings, the disconnect between shares and the total GDP of the US is also correcting but as you can see below, it has only returned to the PEAK of the pre GFC.

So whilst markets have had a very bad run this last month, they still historically have potentially a lot further to fall. Governments will continue to throw more and more new currency at this to manage the damage but that won’t stop the inevitable outcome of shutting down businesses and a broken supply chain. What it does is expand money supply potentially at an unprecedented pace. Yet again we are throwing more debt and more stimulus at a crisis borne of exactly that. COVID was simply the prick of the bubble.

As we discussed last week, gold and silver may initially struggle against the broad scale liquidation of assets and the flight to USD. But that same increase in fiat currency (and the inflationary pressures that must ensue) and the same further capitulation of markets to deeper lows, has historically seen an epic rotation into the world’s oldest safe havens of gold and silver, and quite potentially the newest uncorrelated, ‘hard’ asset of bitcoin.

On a personal note I want to thank the many who have understood and expressed support for our decision to close our physical store today. It was not a decision we took lightly nor one we wanted to do. Rest assured we have everyone’s best interest at heart and will do all we can to help you all through this extraordinary time.