Bank Bail-ins in Australia – Why your cash isn’t safe

News

|

Posted 19/07/2019

|

111750

Is your money really safe in a bank? One of the key outcomes of the G20 Summit held in Brisbane in 2014 was the agreement amongst those nations around the Bank for International Settlements’ (BIS) Financial Stability Board bail-in provisions. A bail-in creates a write off or conversion into shares (in a failing bank) of what that bank owes to unsecured creditors, instead of the government bailing the bank out (as was the case during the GFC). As a bank depositor, you are an unsecured creditor of that bank. So, to be clear, this means that the bank can write off (take) your deposit, or a percentage of it, or use your deposit to buy shares in their failing business which you would then own a part of. Congratulations!

Back in 2018 we wrote this article when very quietly on the 14th of February the senate (the 8 who were present at least…) passed the rushed through Financial Sector Legislation Amendment (Crisis Resolution Powers And Other Measures) Bill 2017. Whilst the Treasury and other agencies involved stated it was not the “intention” for this bill to capture depositors, the bill was rushed through before One Nation could move their intended motion to have the bill explicitly exclude depositors.

Specifically, courtesy of Citizens Electoral Council:

“One Nation Senators had attempted to insert a provision into the Act before its passing to ensure that its intention was clear and that it did not apply to deposits as was being contended by the Commonwealth Government. After the Senators notified the Government that they intended to move an amendment to the Bill to explicitly exclude deposits from being bailed in, the government offered to check the wording of their amendment, and while the Senators waited for the response, the government rushed the bill through the Senate and into law while the Senators were out of the chamber, and with only eight Senators present in the Chamber.”

Last month a NSW solicitor, Robert Butler (who is also a member of the CEC) critically analysed this legislation together with the terms of the major banks that we all sign up to when opening an account.

In summary, he finds that:

“At a minimum, the Act empowers APRA to bail in so-called Hybrid Securities - special high-interest bonds evidenced by instruments which by their terms can be written off or converted into potentially worthless shares in a crisis.

However, the Act also includes write-off and conversion powers in respect of “any other instrument”. The Government has contended that these words do not extend to deposits, on the basis that the power only applies to instruments that have conversion or write-off provisions in their terms, which deposit accounts do not. However, the reference to “any other instrument” would be unnecessary if the power only applied to instruments with conversion or write-off provisions; moreover, banks are able to change the terms and conditions of deposit accounts at any time and for any reason, including on directions from APRA to insert conversion or write-off provisions, which would thereby bring them within the specific terms of the write-off or conversion provisions of the Act.”

He firstly looks at that definition of “instrument” which political defenders of the Act say doesn’t include depositor’s funds but is not defined in the Act. The explanatory notes however state this inclusion goes to “leaving room for future changes to APRA's prudential standards, including changes that might refer to instruments that are not currently considered capital under the prudential standards.” Additionally, a “financial instrument” is defined by Australian Accounting Standard AASB132 as "any contract that gives rise to a financial asset of one entity and a financial liability or equity instrument of another entity."

When you deposit money into a bank you are entering into a contract whereby you hand over a financial asset that is then a financial liability for the bank (to pay you back in the future). That quite clearly sits within that Accounting Standard definition. Fractional Reserve Banking then allows the bank to loan out all but 10% of that deposit, which compounds not only the profit to the bank, but also your concern around being an unsecured creditor.

Secondly, he states (supported by evidence) that notwithstanding current definitions etc, banks have a very clear ability to change the terms and conditions upon which you entered when depositing your funds and without notice. APRA can therefore instruct the distressed bank to change the conditions to remove any “instrument” definition ambiguity, and even do so secretly as allowed by the APRA Act.

Such analysis combined with the reluctance of the government to change the legislation to specifically exclude deposits (as they promised at the G20 Summit) surely justifies the position that bail-in laws on deposits currently exist in this country.

So let’s then look at the scenario of a major financial crisis or housing crash. With Fractional Reserve Banking the bank is allowed to turn 90% of that deposit liability of yours into loans (which then sit as assets on the bank’s balance sheet) and retain just 10% in cash in their accounts. They secure those loans with collateral, and in Australia the vast majority of this is in the form of housing mortgages. If those assets securing the loans become worth less than the loan, this creates a significant crisis for the bank involved. The bank now has more liabilities than assets and is technically insolvent. Your full deposit is one of those liabilities (barring the 10% they “keep”), and quite a liquid one at that. At the same time, panic would ensue with people withdrawing their cash deposits en masse – a so called “bank run”. When everyone wants their cash and the bank only kept 10%, they need to start selling assets to free up the cash on demand, and all that is left is the distressed property which needs to be sold into a free-falling market.

You can see how the dynamics of the death spiral unfold in this scenario, and this is exactly what happened throughout the Great Depression and more recently in Cyprus and Greece. During the GFC governments simply printed money and gave it to the banks to stop the spiral. Bail-ins mean that is no longer on the table. So, the bank needs to take what it can from its creditors, and as we have shown, that is you.

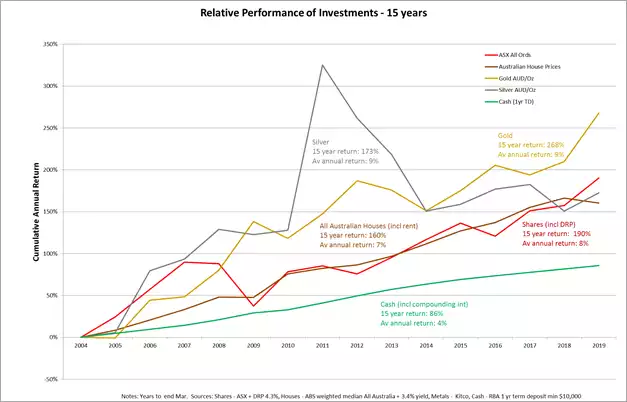

This realisation is becoming more widely understood and at Ainslie we are seeing quite large, “sophisticated” money getting out of the banks and into gold and silver bullion for this very reason. That decision just became a whole lot easier recently as the banks aren’t even paying you much via interest for the privilege of lending 90% of your money out as soon as they get it. To reinforce this point, check out the comparison of cash on term deposit (with interest compounding) in a bank compared to gold and silver over the last 15 years updated to today.

Finally, if you haven’t yet seen it (including this chart) our all-new ‘Why Buy Bullion’ brochure is now on our website here or in physical form in our office.

You can read the bail-in legal analysis in its entirety here.