BIS veteran says global credit excess worse than pre-Lehman

News

|

Posted 18/09/2013

|

2609

The Swiss-based `bank of central banks’ said a hunt for yield was luring investors en masse into high-risk instruments, “a phenomenon reminiscent of exuberance prior to the global financial crisis”.

This is happening just as the US Federal Reserve prepares to wind down stimulus and starts to drain dollar liquidity from global markets, an inflexion point that is fraught with danger and could go badly wrong.

“This looks like to me like 2007 all over again, but even worse,” said William White, the BIS’s former chief economist, famous for flagging the wild behaviour in the debt markets before the global storm hit in 2008.

“All the previous imbalances are still there. Total public and private debt levels are 30pc higher as a share of GDP in the advanced economies than they were then, and we have added a whole new problem with bubbles in emerging markets that are ending in a boom-bust cycle,” said Mr White, now chairman of the OECD’s Economic Development and Review Committee.

The BIS said in its quarterly review that the issuance of subordinated debt -- which leaves lenders exposed to bigger losses if things go wrong -- has jumped more than threefold over the last year to $52bn in Europe, and jumped tenfold to $22bn in the US.

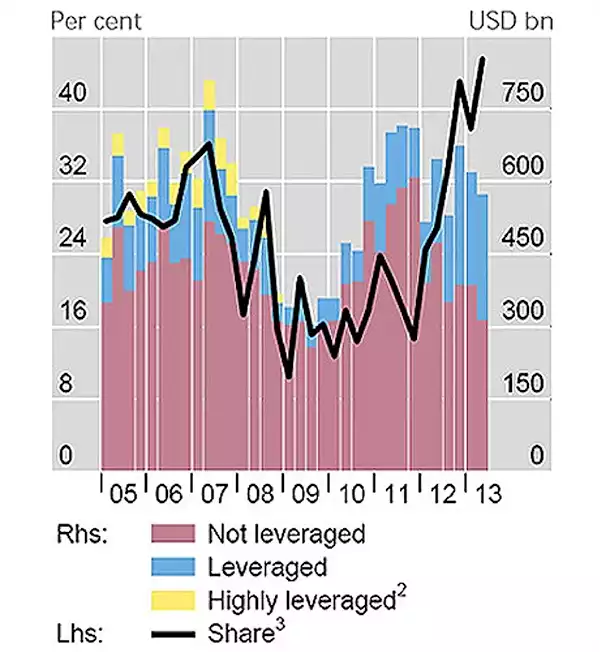

The share of “leveraged loans” used by the weakest borrowers in the syndicated loan market has jumped to an all-time high of 45pc, ten percentage points higher than the pre-crisis peak in 2007-2008.

Share of high risk leveraged loans now greater than 2007

The BIS said investors are snapping up “covenant-lite” loans that offer little protection to creditors, as well as a form of hybrid capital for banks known as CoCos (contingent convertible capital instruments) that switch debt into equity if bank capital ratios fall too low. While CoCos help shield taxpayers from losses in a banking crisis by leaving private creditors with more of the risk, the recent appetite for such an instrument is also a warning sign.

The BIS said interbank credit to emerging markets has reached the “highest level on record” while the value of bonds issued in off-shore centres by private companies from China, Brazil and other developing nations exceeds total issuance by firms from rich economies for the first time, underscoring the sheer size of the debt build-up in Asia, Latin Africa, and the Mid-East.

Claudio Borio, the BIS research chief, said the ructions in emerging markets since the Fed turned hawkish in May is a warning to investors that they must tread with care. “Global financial markets have reacted very strongly. If there were any doubts about the strength of international policy spillovers, they have now been put to rest,” he said.

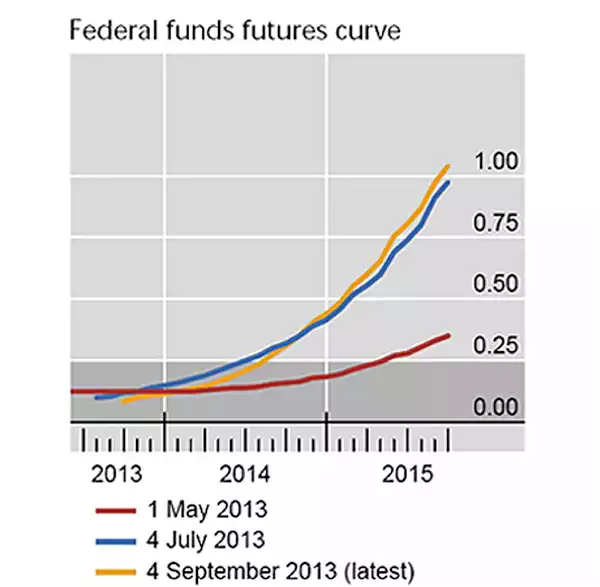

How Bernanke signal has pushed up long term rates

Mr Borio said nobody knows how far global borrowing costs will rise as the Fed tightens or “how disorderly the process might be”.

“The challenge is to be prepared. This means being prudent, limiting leverage, and avoiding the temptation of believing that the market will remain liquid under stress, the illusion of liquidity,” he said.

The BIS enjoys great authority. It was the only major global body that clearly foresaw the global banking crisis, calling early for a change of policy at a time when others were being swept along by the euphoria of the era.

Mr White said the five years since Lehman have largely been wasted, leaving a global system that is even more unbalanced, and may be running out of lifelines. “The ultimate driver for the whole world is the US interest rate and as this goes up there will be fall-out for everybody. The trigger could be Fed tapering but there are a lot of things that can go wrong. I very am worried that Abenomics could go awry in Japan, and Europe remains exceedingly vulnerable to outside shocks.”

Mr White said the world has become addicted to easy money, with rates falling ever lower with each cycle and each crisis. There is little ammunition left if the system buckles again. “I don’t know what they will do: Abenomics for the world I suppose, but this is the last refuge of the scoundrel,” he said.

The BIS quietly scolded Bank of England Governor Mark Carney and his eurozone counterpart Mario Draghi, saying the attempt to use “forward guidance” to hold down long-term rates by rhetoric alone had essentially failed. “There are limits as to how far good communications can steer markets. Those limits have become all too apparent,” said Mr Borio.