Australia’s “Uncharted Territory”

News

|

Posted 12/12/2018

|

5570

RBA Deputy Governor, Guy Debelle, this week described the bank as being in “uncharted territory” as it grapples with how to respond to the paradox of falling house prices against solid employment and reasonable economic growth.

The latter took a hit last week when the Q3 GDP print demonstrably missed expectations at just 2.8% against 3.5% expected. It prompted him to say the next move in interest rates is "more likely up than down, though it is some way off" but openly proffered that if that were not the case, if indeed the GDP continued to soften and house prices continued to fall, that there was “still scope for further reductions in the policy rate”. He even discussed implementing their own quantitative easing (money printing) program off the learnings from other central banks such as the Fed, ECB and BoJ.

As we have repeatedly warned (most recently here) a property crash in Australia extends well beyond owners of property. Our banks are 25% of our sharemarket and they are heavily exposed. They are also highly homogenous given their monopoly. Debelle warned (via AFR):

“"The Australian banks' similarity is not so obviously beneficial in the current circumstance. Their similar behaviour and similar reaction functions to events such as falling house prices run the risk of amplifying the downturn in the housing market," he said.

"The crisis very much demonstrated the critical importance of keeping the lending flowing. The lesson is that countries that did that fared better than countries that didn't. That lesson is relevant to the situation today in Australia, where there is a risk that a reduced appetite to lend will overly curtail borrowing with consequent effects for the Australian economy."

He concluded that "leverage matters", because it can turn a manageable macro event "into a very hard to manage crisis".

"But the questions of how much debt is enough and how much is too much remain unresolved."”

Confidence inspiring stuff.... A debt borne crisis can be averted if we maintain the supply of yet more debt…. But we’re not sure how much is too much….

Enter the OECD this week with the release of their latest assessment of the Australian economy. Whilst they maintain the current housing correction should see a soft landing they warned a “risk of a hard landing remains”. To avert the hard landing they go on to recommend the RBA start raising interest rates off the current 1.5% that has been the floor since August 2016 and arguably fuelled the housing bubble further. From the report:

“Australia’s housing market is a source of vulnerabilities due to elevated prices and related household debt. A direct hit to the financial sector from a wave of mortgage defaults is unlikely……However, if house prices collapse consumer spending could suffer, via negative impact on wealth, including from exposures to bank shares, which would encourage deleveraging. Together with reduced housing-related expenditures, this would put pressure on the whole economy.”

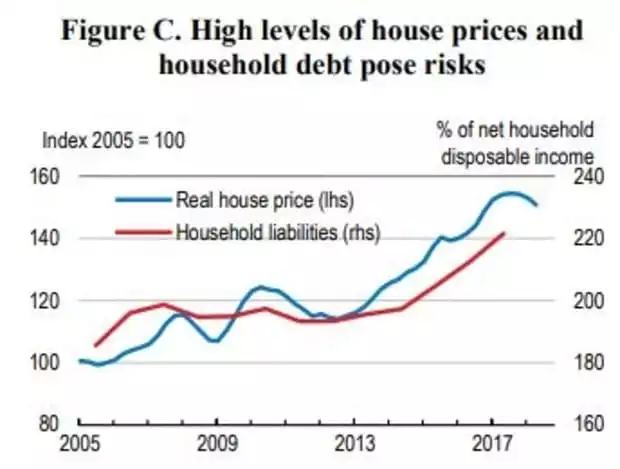

They point to the softening of pricing coinciding with unrelenting debt increases:

Adding to concern about the ‘softness’ of the landing, the report coincided with CoreLogic’s latest prices report showed another 0.5% fall for Sydney taking the ‘peak to current’ fall to 10%, surpassing the previous record during the ‘recession we had to have’ in 1991 of 9.6% and is the highest since they started since 1980. The OECD also conceded its research shows that in such cases “soft landings are rare”.

For global context Australia is most certainly not alone with house prices on decline in other major markets, most notably now being joined by the US: